My uncle took a life insurance policy 20 years ago. He paid ₹18,000 a year for 20 years — ₹3,60,000 total. When the policy matured, he received ₹4,20,000 back. He was thrilled. He told everyone he ‘made money’ from insurance.

The problem? He had only ₹5 lakh of life cover for those 20 years. With a wife and two children depending on his income, ₹5 lakh would have lasted his family maybe 3 months. And if you calculate the actual return on his ₹3,60,000 investment — it worked out to about 3.8% per year. Inflation was 6% during the same period.

He didn’t make money. He lost purchasing power while being dangerously underinsured.

This story plays out in tens of millions of Indian families. Let me explain why — and what you should do instead.

The One-Line Difference That Changes Everything

| Term insurance = pure protection. Cheap, high coverage, nothing back if you survive. Traditional life insurance = protection + forced savings. Expensive, low coverage, some money back. For most people, term insurance is the right answer. |

What Is Term Insurance?

Term insurance is the simplest form of life insurance. You pay a fixed annual premium for a defined period — say 30 years. If you die during this period, your nominee receives the sum assured (e.g. ₹1 crore). If you survive the full term, you receive nothing.

That ‘nothing back’ part puts many people off. But here’s the logic: the purpose of insurance is to protect your family against financial loss if you die. It is not an investment. Mixing protection with investment creates a product that does both poorly.

Because term insurance offers pure risk cover with no savings component, the premium is dramatically lower. A healthy 28-year-old non-smoker can get ₹1 crore of term insurance in India for ₹700–₹900 per month through an IRDAI approved insurance company. That’s less than most people spend on eating out.

What Is Traditional Life Insurance?

Traditional life insurance — also called endowment plans, money-back plans, or whole life insurance — combines a death benefit with a savings or investment component. You pay higher premiums, the insurance company invests part of it, and at the end of the policy term (or on death), you or your nominee receive a payout.

The most widely known provider of these products is LIC (Life Insurance Corporation of India). LIC policy premiums and maturity benefits are deeply embedded in Indian family financial planning — mostly because LIC agents have been selling these products for decades to anyone who would listen.

The appeal is obvious: ‘You’ll definitely get something back.’ The reality is more complicated.

The Real Cost Comparison — Same Person, Two Products

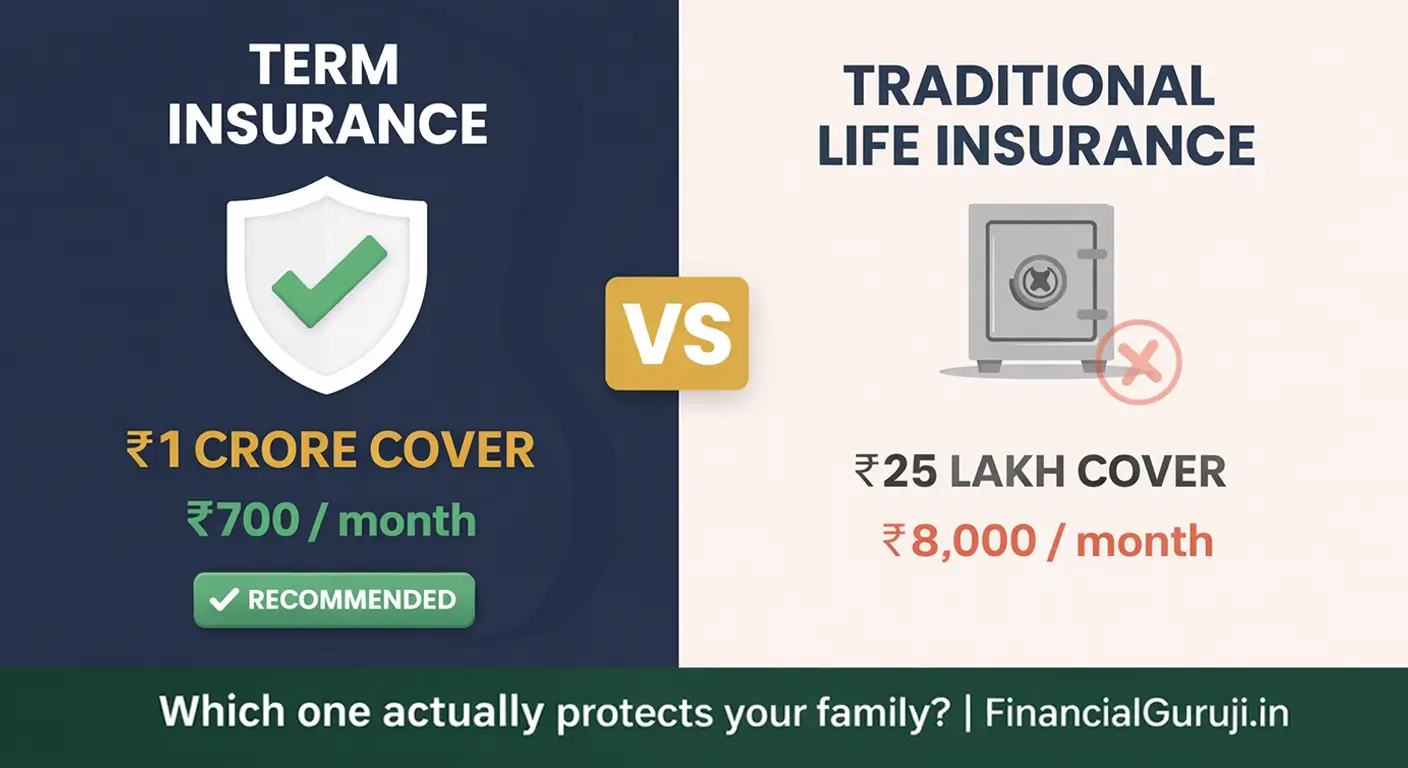

Let’s take a 30-year-old salaried employee, Vikram, with a wife and two young children. Annual income: ₹10 lakh. He needs to ensure his family is protected.

| Term Insurance (₹1 Crore) | Endowment Plan (LIC Jeevan Anand) | |

| Annual premium | ~₹10,000–₹14,000 | ~₹90,000–₹1,10,000 |

| Sum assured (death) | ₹1,00,00,000 | ₹25,00,000 |

| Policy term | 30 years | 30 years |

| Maturity benefit | Nil (pure term plan) | ~₹50,00,000 (approx) |

| Return on premium | NA — pure protection | ~4.5–5.5% CAGR |

| Inflation-adj. return | NA | Negative (inflation ~6%) |

| Total premium paid | ~₹3,00,000–₹4,20,000 | ~₹27,00,000–₹33,00,000 |

| Vikram’s endowment plan gives him 25 lakh of cover for 27–33 lakh in premiums. His term plan gives him 1 CRORE of cover for 3–4.2 lakh total. The endowment plan costs 8x more for 1/4th the coverage. This is why financial advisors universally recommend ‘buy term invest the rest’. |

Buy Term Invest the Rest — The Superior Strategy

The ‘buy term invest the rest’ principle works like this:

- Buy a ₹1 crore term plan for ~₹12,000/year

- Take the premium difference you would have paid for an endowment plan (~₹90,000/year)

- Invest that ₹90,000 annually in a mutual fund SIP (12% expected CAGR)

- After 30 years: SIP corpus ≈ ₹2.7 crore

Compare this to the endowment plan maturity benefit of ~₹50 lakh. The ‘buy term invest the rest’ approach produces ₹1 crore of life cover PLUS ₹2.7 crore of wealth — versus ₹25 lakh cover and ₹50 lakh maturity. The difference is staggering.

Use the Life Insurance Calculator and SIP Calculator on this site to run these numbers for your own age and income.

Term Insurance Claim Settlement Ratio — Why This Number Matters

Before choosing any term insurance plan India, always check the claim settlement ratio (CSR) — the percentage of death claims that the insurer actually paid out in the previous year. IRDAI publishes this data annually.

| Insurer | Claim Settlement Ratio (2023-24) | Individual Death Claims Settled |

| LIC | 98.7% | Very high volume |

| Max Life Insurance | 99.5% | High |

| HDFC Life Insurance | 99.3% | High |

| ICICI Prudential Life | 98.5% | High |

| Tata AIA Life | 99.1% | High |

| SBI Life Insurance | 96.7% | High volume |

Any insurer with a claim settlement ratio above 97% is generally reliable for a best term insurance plan India selection. Don’t choose purely on price — a slightly higher premium at a 99%+ CSR insurer is worth the peace of mind.

How Much Term Insurance Do You Actually Need?

The most common question after ‘what is term insurance’ is ‘how much life insurance do I need’. The standard formula:

| Required coverage = (Annual income × 15) + Outstanding loans + Children’s education corpus needed |

| Annual Income | Formula Calculation | Recommended Cover |

| ₹5 lakh | ₹5L × 15 = ₹75L + any loans | Minimum ₹75 lakh, ideally ₹1 crore |

| ₹8 lakh | ₹8L × 15 = ₹1.2Cr + loans | ₹1 crore to ₹1.5 crore |

| ₹12 lakh | ₹12L × 15 = ₹1.8Cr + loans | ₹1.5 crore to ₹2 crore |

| ₹20 lakh | ₹20L × 15 = ₹3Cr + loans + education | ₹2 crore to ₹3 crore |

A ₹1 crore term plan coverage amount is the practical minimum for a salaried employee with dependents in 2026. The premium difference between ₹50 lakh and ₹1 crore is only ₹2,000–₹3,000/year — always buy the higher cover.

Term Insurance Riders — What to Add, What to Skip

Term insurance riders are add-on benefits you can attach to your base plan for an extra premium. Not all are worth buying.

| Rider | What It Covers | Worth Buying? | Cost |

| Critical Illness Rider | Lump sum on diagnosis of cancer, heart attack, stroke etc. | ✅ Yes — very useful | ₹2,000–₹5,000/yr extra |

| Accidental Death Benefit | Extra payout if death is due to accident | ✅ Yes — cheap add-on | ₹500–₹1,000/yr extra |

| Waiver of Premium | Premiums waived if you become disabled | ✅ Yes — good safety net | ₹500–₹800/yr extra |

| Return of Premium (TROP) | Get all premiums back if you survive | ❌ Skip — 2-3x premium cost | Very expensive |

| Accidental Disability Rider | Income if permanently disabled due to accident | ✅ Consider if manual work | ₹800–₹1,500/yr extra |

Critical illness rider is the most important term insurance rider India to add. Critical illness treatment costs in India (cancer: ₹5–20 lakh, heart bypass: ₹4–8 lakh) can devastate a family’s finances even if the breadwinner survives. A rider that pays ₹25–50 lakh on diagnosis costs very little in addition to term premiums.

How to Buy Term Insurance Online in India — 2026

Online term insurance India is 20–30% cheaper than offline policies bought through agents. The process is fully digital and typically takes 30–60 minutes.

- Compare plans on Policybazaar, Ditto Insurance, or InsuranceDekho

- Check claim settlement ratio for shortlisted insurers (IRDAI website or aggregator)

- Select sum assured (minimum ₹1 crore recommended)

- Choose policy term — cover yourself until age 65–70, not just 40 or 50

- Add critical illness and accidental death riders

- Use the term insurance premium calculator on comparison sites to finalise

- Apply online — fill health declaration honestly (non-disclosure is grounds for claim rejection)

- Medical test may be required for high coverage or age above 35 — insurer arranges this

- Policy document issued digitally within 3–7 days

| Always disclose pre-existing health conditions honestly during application. Non-disclosure is the most common reason insurers reject death claims. An honest application with slightly higher premium is infinitely better than a claim your family cannot collect. |

Term Insurance Age Limit — When to Buy

The earlier you buy, the cheaper the premium — permanently. Term insurance premiums are locked at the age of purchase and don’t increase year on year (unlike health insurance).

| Age at Purchase | Annual Premium for ₹1 Crore (Non-smoker, Male, 30yr Term) |

| 25 years | ~₹7,000–₹9,000/year |

| 30 years | ~₹10,000–₹13,000/year |

| 35 years | ~₹14,000–₹18,000/year |

| 40 years | ~₹22,000–₹28,000/year |

| 45 years | ~₹35,000–₹45,000/year |

The term insurance age limit for most insurers is 65–70 years (maximum entry age) with coverage available until 75–85 years. But buying at 25 instead of 35 saves approximately ₹1,20,000–₹1,50,000 in total premiums over a 30-year policy.

If you have dependents and you’re between 22–40 years old — buy term insurance this week. Not next month. This week.

Should You Surrender Your Existing LIC Policy?

If you already have an endowment or money-back LIC policy, the question of whether to surrender it is complicated and depends on how many years of premiums you’ve paid.

- Paid less than 3 years: Surrender value is very low or zero — consider stopping and starting fresh with a term plan

- Paid 5–10 years: Calculate the surrender value vs the future premiums you’d pay — may be worth continuing to maturity

- Paid 15+ years, near maturity: Continue to maturity — the bulk of the return is in the final years

- Policy with loan against it: Clear the loan first, then evaluate surrender

For a personalised decision, consult a SEBI-registered fee-only financial planner — not an LIC agent, who has a financial incentive to keep you in the policy.

→ Use our Life Insurance Calculator to find the right coverage amount for your income and family

Frequently Asked Questions

What is the best term insurance plan in India for 2026?

Plans from Max Life, HDFC Life, Tata AIA, and ICICI Prudential consistently rank among the best term insurance plan India options based on claim settlement ratio (99%+), premium competitiveness, and policy flexibility. Compare on Policybazaar or Ditto using the term insurance premium calculator — the right plan depends on your age, health, and coverage needs.

Is term insurance worth buying if I already have group insurance from my employer?

Employer group insurance is not sufficient — it typically covers 3–5x salary (₹15–30 lakh for most employees), lapses the moment you leave the job, and offers no flexibility. A personal term insurance policy of ₹1 crore+ is essential regardless of employer coverage.

What happens to term insurance if I stop paying premiums?

If you miss premium payments beyond the grace period (usually 30 days), the policy lapses — your coverage ends. Most insurers allow policy revival within 2–5 years of lapsing by paying overdue premiums plus interest. After the revival window, the policy cannot be reinstated.

Can a smoker get term insurance in India?

Yes, but at significantly higher premiums — typically 30–50% more than a non-smoker rate. Always declare smoking status honestly. If you quit smoking for 12+ months before applying, you may qualify for non-smoker rates with a medical test.

What is return of premium (TROP) term insurance and should I buy it?

Return of premium term insurance returns all your premiums at maturity if you survive. The catch: premiums are 2.5–3x higher than a regular term plan. The extra premium is better invested in a mutual fund SIP — the corpus you’d build is far larger than the returned premiums. Most financial advisors recommend skipping TROP and choosing pure term instead.

What is the term insurance claim settlement process in India?

After the policyholder’s death: nominee contacts the insurer with the death certificate and policy documents → insurer assigns a claim manager → documents are verified → if no discrepancies, claim is settled within 30 days (IRDAI mandate). For IRDAI approved insurance companies with 99%+ CSR, the process is smooth. Keep your nominee informed about the policy location and sum assured.