Rahul spent Rs 40,000 on his credit card in December — a mix of electronics, groceries, and a weekend trip. He paid the minimum amount due of Rs 2,000 and thought he had handled it responsibly.

He had not. By the time he checked his next statement, the outstanding balance was Rs 39,200. He had paid Rs 2,000 but the interest charged was Rs 1,200. He had reduced his debt by only Rs 800.

At this rate — paying only the minimum — it would take Rahul 4 years and 3 months to clear that Rs 40,000. He would pay Rs 19,600 in interest on top of the original amount. For a month’s spending that felt like normal life expenses.

This is the credit card interest trap. It is legal, it is everywhere, and most Indians do not fully understand how it works until they are inside it.

Credit Card Interest Rate in India — The Real Numbers

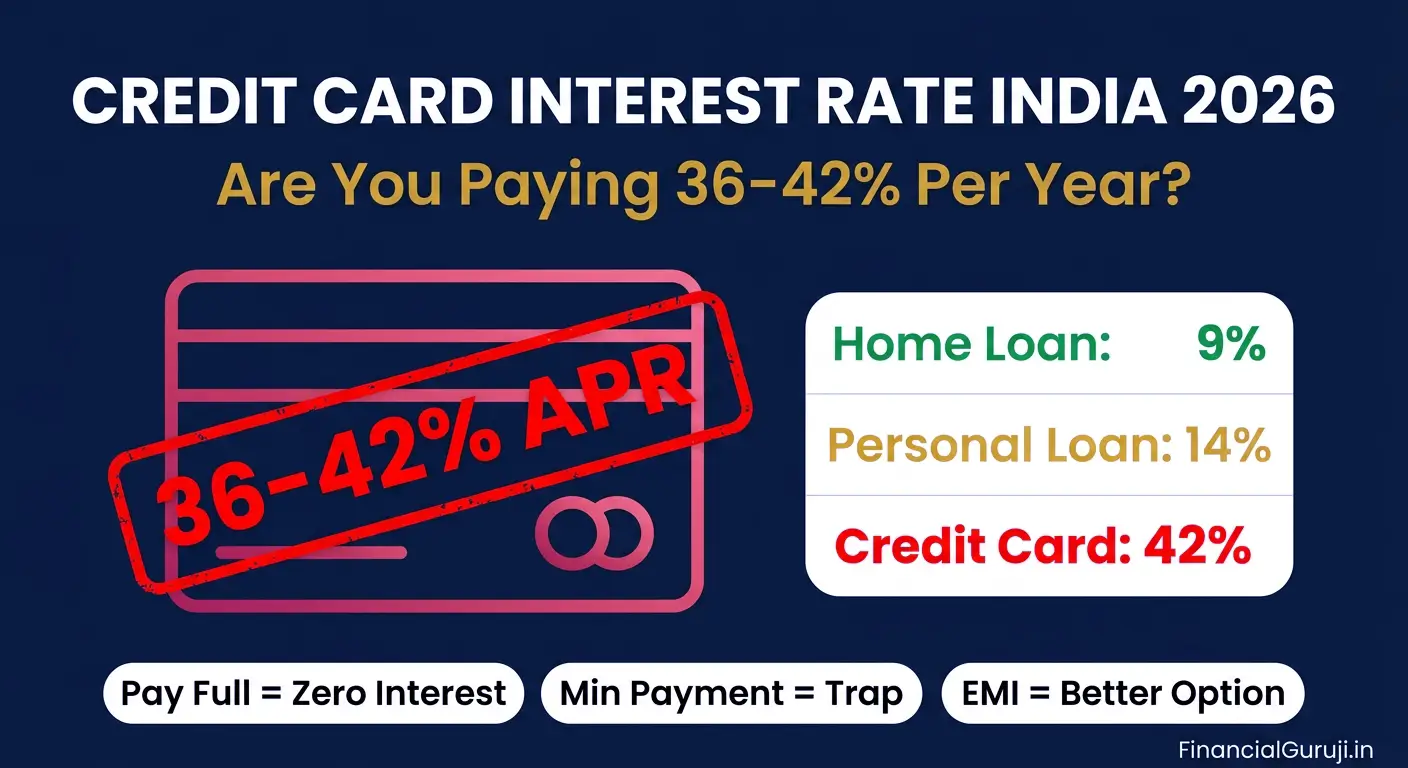

Credit card APR in India ranges from 36% to 42% per year — the highest interest rate of any mainstream financial product available to consumers. For comparison:

| Loan Type | Annual Interest Rate | Monthly Rate |

| Credit card (revolving balance) | 36% to 42% per year | 3% to 3.5% per month |

| Personal loan | 11% to 18% per year | 0.9% to 1.5% per month |

| Home loan | 8.5% to 9.5% per year | 0.7% to 0.8% per month |

| Car loan | 9% to 12% per year | 0.75% to 1% per month |

| Gold loan | 9% to 14% per year | 0.75% to 1.2% per month |

| EPF / PPF | 8.25% / 7.1% return | Positive return for you |

| Warning: Credit card interest at 36-42% per year means your debt nearly doubles every 2 years if you only pay minimums. No investment in India reliably returns 36% per year. Carrying a credit card balance is the single most financially destructive thing a salaried Indian can do. |

How Credit Card Interest Is Calculated — Step by Step

Most people do not understand that credit card interest calculation in India is not simple monthly interest. It is daily compounding from the transaction date — not from the due date.

The Billing Cycle and Grace Period

Every credit card has a billing cycle — typically 28 to 31 days. At the end of each cycle, you receive a statement with the total amount due and the minimum amount due. You then have a grace period — usually 18 to 25 days — to pay the full amount without any interest charges.

Credit card grace period India: If you pay the complete statement balance before the due date, you pay zero interest. The credit card is essentially a free 45 to 55 day loan. This is how disciplined credit card users pay no interest ever.

When Interest Starts — The Key Trigger

Interest begins the moment you do not pay the full statement balance by the due date. Not from the due date — from the original transaction date, retroactively.

| Scenario | Interest Charged? | From When |

| Pay full statement balance by due date | Zero — free credit period applies | NA |

| Pay minimum amount due only | 3% to 3.5% per month on full outstanding | From original purchase date |

| Pay partial amount (more than minimum) | 3% per month on unpaid balance | From original purchase date |

| Miss due date entirely | 3-3.5% interest plus late payment charge | From original purchase date |

| Next month purchases — if previous unpaid | No grace period — interest from day 1 | From new purchase date |

| The most expensive credit card mistake: paying partial payment instead of full. If your statement is Rs 30,000 and you pay Rs 29,000 — you pay interest on the full Rs 30,000 from purchase dates, not just the Rs 1,000 unpaid. Partial payment does NOT preserve the grace period on the paid portion. |

The Minimum Payment Trap — Real Calculation

Credit card minimum payment is designed to keep you in debt as long as possible. Here is the math on a real Rs 50,000 balance:

| Repayment Strategy | Monthly Payment | Months to Clear | Total Interest Paid |

| Minimum only (2-5% of balance) | Rs 1,500 to Rs 2,500 (declining) | 54 months | Rs 24,800 |

| Fixed Rs 5,000/month | Rs 5,000 | 12 months | Rs 8,600 |

| Fixed Rs 10,000/month | Rs 10,000 | 6 months | Rs 3,900 |

| Full payment immediately | Rs 50,000 | 0 months | Rs 0 |

Paying minimum only costs you Rs 24,800 in interest over 54 months — nearly 50% extra on your original Rs 50,000 spending. Paying Rs 10,000 per month costs only Rs 3,900 and clears in 6 months. The difference between strategies is enormous.

Credit Card Interest Rate — Bank Wise India 2026

| Bank / Card | Monthly Interest Rate | Annual Rate (APR) | Late Payment Charge |

| HDFC Bank Credit Cards | 3.6% per month | 43.2% | Rs 100 to Rs 1,300 (slab-based) |

| SBI Credit Cards | 3.5% per month | 42% | Rs 400 to Rs 1,300 |

| ICICI Bank Credit Cards | 3.5% per month | 42% | Rs 100 to Rs 1,200 |

| Axis Bank Credit Cards | 3.6% per month | 43.2% | Rs 500 to Rs 1,200 |

| Kotak Mahindra Cards | 3.5% per month | 42% | Rs 100 to Rs 1,000 |

| Yes Bank Credit Cards | 2.99% per month | 35.88% | Rs 100 to Rs 1,100 |

| IDFC First Credit Cards | 0.75% to 3.5% | 9% to 42% | Rs 100 to Rs 1,000 |

| AU Small Finance Bank | 1.99% to 3.49% | 24% to 42% | Rs 100 to Rs 750 |

| Tip: IDFC First and AU Small Finance Bank offer lower interest rates than large private banks — especially for their premium card variants. If you occasionally carry a balance, these are worth considering. However, the best strategy remains paying in full every month regardless of rate. |

Credit Card Late Payment Charges — What They Actually Cost

Missing the due date triggers two separate charges: interest on outstanding balance AND a flat late payment fee. Both apply simultaneously.

| Outstanding Balance | Late Payment Charge (typical) | Plus Interest (3.5%/month) | Total Extra Cost Month 1 |

| Up to Rs 500 | Rs 100 | Rs 17 | Rs 117 |

| Rs 501 to Rs 5,000 | Rs 500 | Rs 122 | Rs 622 |

| Rs 5,001 to Rs 10,000 | Rs 600 | Rs 262 | Rs 862 |

| Rs 10,001 to Rs 25,000 | Rs 800 | Rs 612 | Rs 1,412 |

| Rs 25,001 to Rs 50,000 | Rs 1,100 | Rs 1,312 | Rs 2,412 |

| Above Rs 50,000 | Rs 1,300 | Rs 1,750+ | Rs 3,050+ |

RBI credit card rules 2026: RBI mandates that banks must clearly disclose all charges in the Key Fact Statement (KFS) of each credit card. Banks cannot charge interest rates higher than what is disclosed in the KFS. If you believe you were charged incorrectly, you can raise a complaint with the bank and escalate to RBI Ombudsman.

Credit Card EMI Conversion — Is It Worth It?

Most banks offer to convert large outstanding balances into EMIs at a lower interest rate — typically 12% to 18% per year versus the 36-42% revolving rate. This is called credit card EMI conversion.

| Option | Rs 50,000 outstanding | Total Cost | Verdict |

| Continue as revolving at 42% | Min payment 54 months | Rs 74,800 total | Worst option |

| Convert to 12-month EMI at 14% | Rs 4,485/month EMI | Rs 53,820 total | Much better |

| Convert to 6-month EMI at 14% | Rs 8,710/month EMI | Rs 52,260 total | Best EMI option |

| Personal loan at 12% (6 months) | Rs 8,680/month EMI | Rs 52,080 total | Marginally better |

EMI conversion is significantly better than revolving credit. However, the best option is a personal loan from your bank at 12-14% to pay off the credit card entirely — then close or reduce your credit card limit to avoid repeating the cycle.

Credit card debt consolidation India: If you have balances across multiple cards, a single personal loan to clear all of them simplifies repayment and dramatically reduces total interest paid.

6 Ways to Never Pay Credit Card Interest

- Pay the full statement balance every month — not the minimum, not partial. Full. Set a calendar reminder 3 days before the due date.

- Enable auto-pay for full outstanding balance — most banks offer this via net banking. The entire statement amount is auto-debited on the due date. Zero chance of missing payment.

- Reduce your credit limit — call your bank and lower the limit to 2x your monthly salary. High limits encourage high spending.

- Use the credit card only for planned expenses — groceries, fuel, utility bills with rewards. Not for impulse purchases or items you cannot afford from your bank account this month.

- Never withdraw cash from a credit card — credit card cash advance interest starts from day 1 with no grace period, at the same 36-42% rate plus a cash advance fee of 2.5-3%. This is the most expensive way to borrow money in India.

- Check your statement date vs due date — pay 3-4 days before the due date, not on the last day. Bank processing delays can cause technical late payment marks on your CIBIL record.

How to Get Out of Credit Card Debt — Step by Step

If you are already carrying a credit card balance, here is the priority order:

- Stop using the card for new purchases immediately — use debit card or UPI only

- Call the bank and request a one-time interest waiver — banks sometimes offer this for good customers. Worth asking.

- Check personal loan rates from your salary bank — HDFC, ICICI, SBI all offer instant personal loans to salary account holders at 11-14%. Use this to clear the credit card.

- If personal loan not available, request EMI conversion from the card issuer

- Pay as much as possible above the minimum every month — every extra rupee saves 3.5% per month in ongoing interest

- Once cleared, set up auto-pay for full balance — never carry a balance again

| Tip: The fastest debt payoff method: while clearing credit card debt, pause all non-essential SIP investments temporarily. The 36% interest you are saving beats any SIP return. Clear the card first, restart SIP the next month. |

Use our Credit Card EMI Calculator to see exactly how long your current balance will take to clear — and how much interest you will pay

Frequently Asked Questions

What is the credit card interest rate in India in 2026?

Credit card interest rate India 2026 ranges from 36% to 43.2% per year (3% to 3.6% per month) across major banks. IDFC First and AU Small Finance Bank offer lower rates starting at 9-24% for certain card variants. The rate is applied on the outstanding balance from the original transaction date when you do not pay the full statement amount.

How is credit card interest calculated on partial payment?

If you pay partial payment, interest is charged on the FULL statement balance from the original transaction dates — not just the unpaid portion. Example: Rs 30,000 statement, you pay Rs 25,000. Interest is charged on Rs 30,000 from each purchase date, not just Rs 5,000. Partial payment does not preserve the interest-free grace period on any portion of the bill.

What is the credit card grace period in India?

Credit card grace period India is the interest-free window between your statement date and payment due date — typically 18 to 25 days. If you pay the complete statement balance within this period, zero interest is charged. The full credit period including billing cycle can be 45 to 55 days from purchase date to payment due date.

Is it better to pay minimum due or more on a credit card?

Always pay more than the minimum — ideally the full outstanding. Paying only the minimum on a Rs 50,000 balance takes 54 months and costs Rs 24,800 in interest. Paying Rs 10,000 per month clears it in 6 months for only Rs 3,900 interest. The minimum payment is designed by banks to maximize interest income — it is not designed for your benefit.

Can I negotiate my credit card interest rate with the bank?

Yes — and it works more often than people expect. If you have been a customer for 2+ years with good payment history, call the credit card helpline and request an interest rate reduction. Banks have discretion to reduce rates for valuable customers. Alternatively, request balance transfer to a card with lower APR or apply for personal loan to clear the balance.

What are RBI rules on credit card interest charges in 2026?

RBI credit card rules 2026 require banks to: provide a Key Fact Statement with all charges before card issuance, not charge interest on disputed transactions under investigation, provide a 30-day notice before changing interest rates, and allow customers to close the card within 30 days of rate change without penalty. Banks must also send statement at least 14 days before the due date.