When Ramesh’s daughter Aarohi was born in 2019, a colleague suggested opening a Sukanya Samriddhi account. Ramesh thought about it for a few weeks — it seemed like a government scheme with too many restrictions. He put it off.

His brother Suresh opened an SSY account for his daughter the same year and started depositing Rs 5,000 per month.

In 2026, Suresh’s SSY account has already accumulated over Rs 5.3 lakh — earning 8.2% guaranteed interest, completely tax-free. By the time his daughter turns 21, that account will have grown to approximately Rs 37 lakh from Rs 9 lakh invested. The government adds Rs 28 lakh in interest.

Ramesh missed 7 years of 8.2% compounding. That delay will cost his daughter approximately Rs 12 to 15 lakh at maturity.

If you have a daughter below age 10, this guide is for you.

What is Sukanya Samriddhi Yojana

Sukanya Samriddhi Yojana (SSY) is a government-backed small savings scheme specifically designed for the financial security of the girl child in India. Launched in 2015 under the Beti Bachao Beti Padhao initiative, it offers the highest guaranteed interest rate of any government savings scheme — currently 8.2% per year for Q1 FY 2026-27.

Like PPF, SSY is an EEE scheme — investment qualifies for Section 80C deduction, interest earned is tax-free, and the maturity amount is completely tax-free.

SSY Key Features at a Glance — 2026

| Feature | Details |

| Current interest rate | 8.2% per annum (reviewed quarterly — highest among all small savings schemes) |

| Who can open | Parent or legal guardian of girl child below 10 years of age |

| Maximum accounts per family | One account per girl child, maximum two girls (three if twins/triplets in second birth) |

| Minimum deposit per year | Rs 250 — account stays active |

| Maximum deposit per year | Rs 1,50,000 — same as 80C limit |

| Deposit period | 15 years from account opening date |

| Maturity | 21 years from account opening date OR on marriage after age 18 |

| Tax benefit | EEE — Section 80C deduction + tax-free interest + tax-free maturity |

| Partial withdrawal | Up to 50% of balance allowed after girl turns 18 — for education only |

| Where to open | Post office or any authorised bank — SBI, HDFC, ICICI, Axis, PNB, etc. |

| Account in whose name | In the girl child’s name — operated by guardian till she turns 18 |

SSY Interest Rate 2026 — History and Current Rate

SSY interest rate is set by the government and reviewed every quarter. Here is how it has moved:

| Period | SSY Interest Rate | Remarks |

| FY 2015-16 (launch) | 9.2% | Highest ever rate |

| FY 2018-19 | 8.5% | Gradual reduction |

| FY 2020-21 | 7.6% | Lowest point |

| FY 2023-24 | 8.0% | Rate revised upward |

| FY 2024-25 | 8.2% | Current applicable rate |

| Q1 FY 2026-27 (Apr 2026) | 8.2% | Unchanged — check NSIA for latest |

| Even at the lowest SSY rate of 7.6%, SSY outperformed most bank FDs and PPF (7.1%) on post-tax returns since SSY interest is completely tax-free. At 8.2%, the gap is even wider. For a 30% tax bracket investor, a 8.2% tax-free return equals a 11.7% pre-tax FD rate — no FD offers this. |

SSY Maturity Amount — Real Calculations

The maturity amount depends on how much you deposit and when you start. All calculations below use 8.2% interest rate and assume deposits made at the start of each financial year.

| Monthly Deposit | Annual Deposit | Total Invested (15 yrs) | Maturity at 21 Years | Tax-Free Gain |

| Rs 1,000 | Rs 12,000 | Rs 1,80,000 | Rs 5,40,000 | Rs 3,60,000 |

| Rs 2,500 | Rs 30,000 | Rs 4,50,000 | Rs 13,50,000 | Rs 9,00,000 |

| Rs 5,000 | Rs 60,000 | Rs 9,00,000 | Rs 27,00,000 | Rs 18,00,000 |

| Rs 8,333 | Rs 1,00,000 | Rs 15,00,000 | Rs 45,00,000 | Rs 30,00,000 |

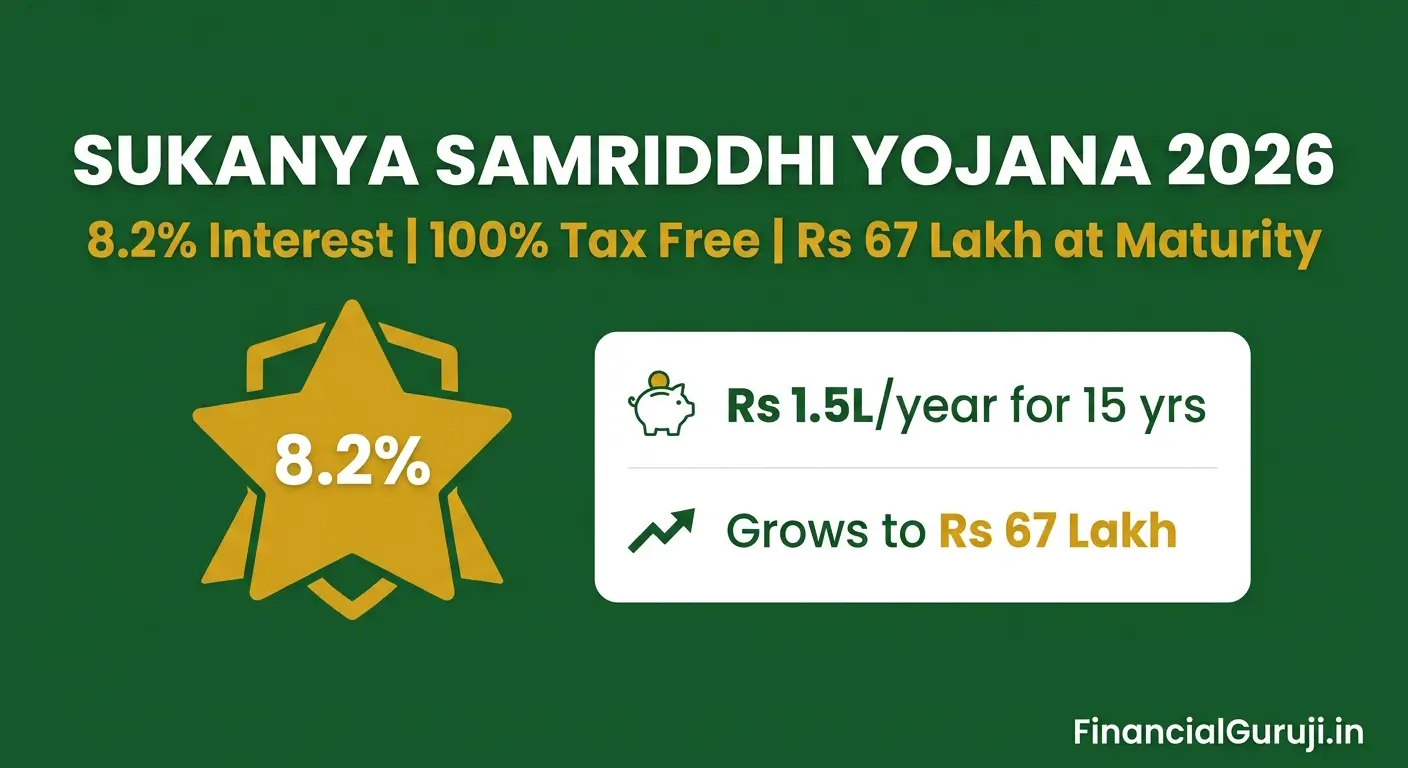

| Rs 12,500 | Rs 1,50,000 | Rs 22,50,000 | Rs 67,34,000 | Rs 44,84,000 |

Maximum SSY investment of Rs 1.5 lakh per year for 15 years grows to approximately Rs 67 lakh at maturity — from Rs 22.5 lakh invested. The government adds Rs 44.8 lakh in interest, completely tax-free.

| Tip: Deposit before April 5th every year to earn interest for the full year on that deposit — same rule as PPF. Depositing on April 5th vs April 30th saves exactly one month of 8.2% interest every year. Over 15 years, this discipline adds approximately Rs 40,000 to Rs 70,000 to the final corpus. |

SSY Deposit Rules — Important Details

Deposit Period vs Maturity Period

This confuses many parents. Deposits must be made for 15 years from account opening. But the account matures at 21 years. For the last 6 years (years 16 to 21), no deposits are required — the existing balance continues earning 8.2% interest automatically.

Example: Account opened in 2026 for a 1-year-old daughter. Deposits made from 2026 to 2041 (15 years). No deposits needed from 2042 to 2047. Account matures in 2047 when daughter turns 21.

| Year Range | Action Required | Interest Earned |

| Years 1-15 (deposit period) | Minimum Rs 250 per year to keep account active — maximum Rs 1.5L | 8.2% on full balance |

| Years 16-21 (silent period) | No deposit needed — account runs automatically | 8.2% on accumulated balance |

| Year 21 (maturity) | Full corpus available for withdrawal — tax-free | Full maturity amount paid |

| Warning: If you miss depositing even Rs 250 in any year during the 15-year deposit period, the account becomes inactive. To reactivate: pay Rs 50 penalty per year of default plus the minimum Rs 250 deposit for each missed year. Reactivation must happen before the deposit period ends. |

SSY Partial Withdrawal Rules

SSY allows partial withdrawal for higher education after the girl turns 18:

- Eligible age: Girl must have completed 18 years OR passed Class 10

- Maximum withdrawal: 50% of the account balance at the end of the previous financial year

- Purpose: Higher education fees only — admission fee, tuition fee

- Proof required: Admission offer letter from educational institution

- Mode: Lump sum or in up to 5 instalments per year

- Remaining balance: Continues earning 8.2% until maturity at 21

Example: Rs 30 lakh balance when daughter turns 18. Maximum partial withdrawal = Rs 15 lakh. This can cover engineering or medical college fees while the remaining Rs 15 lakh continues growing till age 21.

SSY Account — Marriage Before Age 21

If your daughter gets married between age 18 and 21, the SSY account can be closed prematurely on the date of marriage. Full balance is paid out — tax-free. This is the only valid reason for premature closure besides death of account holder or extreme compassionate grounds approved by central government.

SSY Premature Closure Rules

| Reason | Allowed? | Conditions |

| Marriage of girl child after age 18 | Yes — full amount paid | Close on or after marriage date — not before 18 |

| Death of account holder (girl child) | Yes — full amount to guardian | Death certificate required |

| Death of guardian | Yes — if financial hardship proven | Approved case by case |

| Life-threatening illness of girl | Yes — central govt approval | Medical certificate + application |

| Normal premature closure | Not allowed | Account must run to 21 years or marriage |

How to Open SSY Account — Step by Step

- Visit your nearest post office or authorised bank branch (SBI, HDFC, ICICI, Axis, PNB, Bank of Baroda, Canara Bank, or any authorised bank)

- Carry documents: Birth certificate of girl child, Parent/guardian Aadhaar + PAN, Parent/guardian photograph, Filled SSY account opening form (Form 1 — available at branch or download from NSIA website)

- Make initial deposit — minimum Rs 250, maximum Rs 1,50,000

- Receive passbook with account details — keep this safely for all future transactions

- For online deposits: link SSY account to your net banking — most banks allow online top-ups after initial offline opening

| Tip: Open SSY account at a bank rather than post office if you want online deposit convenience. Post office accounts require physical visits for deposits unless you have IPPB (India Post Payments Bank) account linked. SBI, HDFC, and ICICI all support online SSY deposits through net banking. |

SSY Account Transfer Rules

If you relocate to another city, your SSY account can be transferred between post offices or between banks across India — completely free of charge. Submit a transfer request at the current branch with your passbook and ID proof. The account retains all history and interest earnings without any break.

SSY vs PPF — Which is Better for Girl Child

| Factor | SSY | PPF |

| Interest rate | 8.2% (higher) | 7.1% |

| Tax status | EEE — same as PPF | EEE |

| Who can invest | Only for girl child below 10 | Anyone |

| Maturity | 21 years from opening | 15 years (extendable) |

| Deposit period | 15 years | 15 years |

| Max annual deposit | Rs 1.5 lakh | Rs 1.5 lakh |

| Partial withdrawal | 50% after girl turns 18 | 50% from year 7 |

| Premature closure | Only on marriage/death | Not allowed (except death) |

| Liquidity | Lower — longer lock-in | Better — year 7 partial |

| Best for | Dedicated daughter fund | General long-term savings |

| If you have a daughter below 10, SSY is strictly better than PPF for that specific goal — higher rate (8.2% vs 7.1%), same EEE tax treatment, same maximum deposit. The only trade-off is lower liquidity. Use SSY for daughter’s education/marriage fund and PPF for your own retirement savings — both simultaneously. |

Use our SSY Calculator — enter your daughter’s age, monthly deposit, and see the exact maturity amount waiting for her at 21

Frequently Asked Questions

What is the SSY interest rate for 2026?

The SSY interest rate for Q1 FY 2026-27 (April to June 2026) is 8.2% per annum — unchanged from FY 2024-25. This is the highest rate among all government small savings schemes including PPF (7.1%), Post Office MIS (7.4%), and Senior Citizen Savings Scheme (8.2% — same as SSY). Check the National Savings Institute website for the latest quarterly rate.

Can I open two SSY accounts for two daughters?

Yes — one account per girl child, and you can open accounts for maximum two daughters. If your second birth results in twins or triplets, a third account is allowed. Each account has its own separate Rs 1.5 lakh annual deposit limit — so a family with two daughters can invest up to Rs 3 lakh per year across both SSY accounts under Section 80C.

What happens to SSY account if I miss a deposit year?

If you do not deposit the minimum Rs 250 in any financial year during the 15-year deposit period, the account becomes inactive (defaulted). To reactivate: pay Rs 50 per year of default as penalty plus Rs 250 minimum deposit for each missed year. Reactivation must be done before the end of the 15-year deposit period. Interest continues to accrue even during default period.

Can my daughter operate her own SSY account?

Once your daughter turns 18, she can operate the account herself — sign cheques, make deposits, submit withdrawal requests. Before 18, the account is operated by the parent or guardian. At maturity (age 21), the full amount is payable to the daughter directly.

Is SSY better than mutual funds for daughter’s education fund?

SSY at 8.2% tax-free is safer but lower return than equity mutual funds (expected 12-14% CAGR over long term). For a 15-20 year horizon, equity mutual funds historically build larger corpus but with market risk. The ideal approach: SSY for guaranteed foundation (Rs 50K to Rs 1.5L per year) plus equity SIP for additional growth. Do not put everything in one basket for a goal this important.

Can I deposit Rs 1.5 lakh in one go or must it be monthly?

You can deposit in any pattern — monthly, quarterly, annually, or lump sum — as long as the total in a financial year does not exceed Rs 1.5 lakh and is at least Rs 250. A single lump sum deposit of Rs 1.5 lakh before April 5th each year maximises interest earned for that year. Online NEFT deposits are accepted at most banks.