Every January to March, mutual fund platforms see a flood of new ELSS investments. People rushing to fill their Section 80C limit before the financial year closes. Most of them pick whatever shows up first in the search results, or whatever their colleague mentioned in passing.

That is a fine way to save tax. It is a poor way to build wealth. The ELSS fund you pick matters — not for the next 3 years, but for the 15 to 20 years most good investors stay in equity.

This guide covers what ELSS actually is, why it beats every other 80C option for long-term investors, which specific funds have performed well, and what to check before investing in 2026.

What Is ELSS — ELSS Mutual Fund Meaning

ELSS stands for Equity Linked Savings Scheme. It is a category of mutual fund that:

- Invests primarily in equity (stocks) — minimum 80% in equity and equity-related instruments

- Qualifies for Section 80C tax deduction — investments up to Rs 1.5 lakh deductible from taxable income

- Has a 3-year lock-in period per instalment — the shortest lock-in in the entire 80C category

- Is regulated by SEBI — all ELSS funds are SEBI-registered and AMC-managed

The ELSS lock-in period of 3 years means each SIP instalment you invest today can be redeemed after exactly 3 years from that investment date. Not 3 years from when you started the SIP — 3 years from each unit purchase.

Why ELSS Beats Every Other 80C Option in 2026

| 80C Option | Lock-in | Expected Return | Tax on Maturity | Best For |

| ELSS Mutual Fund | 3 years | 12-16% CAGR (market-linked) | 10% LTCG above Rs 1.25L/yr | Long-term wealth + tax saving |

| PPF | 15 years | 7.1% (fixed by govt) | Tax-free (EEE) | Safe, guaranteed savings |

| 5-Year Tax Saving FD | 5 years | 6.5-7.5% (fixed) | Fully taxable as income | Capital protection |

| NSC | 5 years | 7.7% (fixed) | Partially taxable | Conservative investors |

| NPS (80C portion) | Till 60 | 10-12% (market-linked) | Partial tax on exit | Retirement-only corpus |

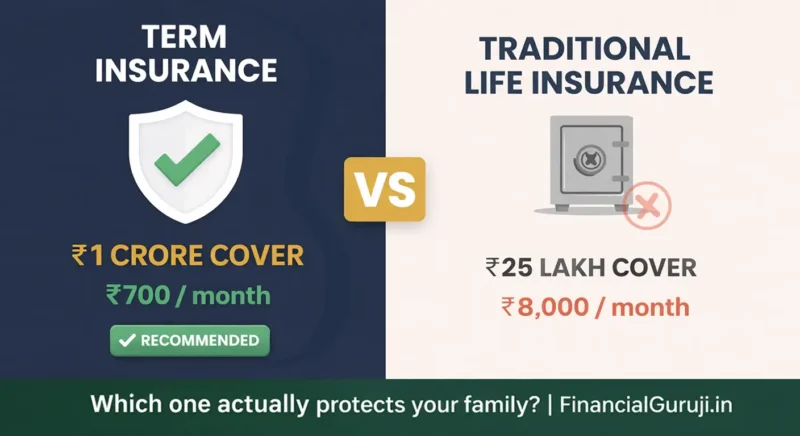

| ULIP | 5 years | Varies, high charges | Mostly tax-free | Generally not recommended |

| ELSS wins on three counts: shortest lock-in (3 years vs 5-15 for others), highest return potential (equity over long term), and lowest effective tax — only 10% LTCG on gains above Rs 1.25 lakh per year. The ELSS capital gains tax structure makes it the most efficient 80C option for taxpayers in the 20-30% slab. |

Top 5 ELSS Funds to Consider in 2026

Selected based on: consistent long-term performance (5-year and 10-year CAGR), expense ratio in direct plan, fund manager track record, AUM stability, and portfolio quality. Past returns do not guarantee future performance — always verify latest data before investing.

1. Mirae Asset ELSS Tax Saver Fund

One of the most consistent ELSS performers in India. Large-cap heavy portfolio with selective midcap exposure. Known for strong risk-adjusted returns — it tends to fall less than peers during corrections and participate well in recoveries.

| Metric | Details |

| Fund Category | ELSS / Tax Saver |

| 5-Year Return | Approx 16-18% CAGR (check AMC site for latest) |

| ELSS Expense Ratio | ~0.5% direct plan | ~1.6% regular plan |

| Portfolio Style | Large-cap biased, quality-focused |

| Minimum SIP | Rs 500 per month |

| Lock-in | 3 years per instalment |

| Best For | Conservative equity investors, first-time ELSS investors |

| Tip: Always choose the Direct Plan. The difference between direct (0.5%) and regular (1.6%) expense ratio on an Rs 1.5 lakh annual investment over 10 years can mean Rs 60,000 to Rs 80,000 extra in your pocket. |

2. Quant Tax Plan

The highest-returning ELSS fund over 3 and 5 years in recent data — but with much higher volatility than peers. Uses a quantitative, data-driven approach with high active share and aggressive sector rotation. Not for the faint-hearted, but the numbers have been exceptional.

| Metric | Details |

| Fund Category | ELSS / Tax Saver |

| 5-Year Return | Approx 22-28% CAGR (very high variance — verify current) |

| ELSS Expense Ratio | ~0.5% direct plan |

| Portfolio Style | High conviction, quant-driven, high turnover |

| Minimum SIP | Rs 500 per month |

| Risk Level | High — can underperform significantly in some periods |

| Best For | Aggressive investors with 10+ year horizon who can stomach volatility |

3. Parag Parikh Tax Saver Fund

Unique among ELSS funds — it holds a mix of Indian equities and select international stocks (primarily US companies like Alphabet and Meta). This gives genuine global diversification within a tax-saving fund, which no other Indian ELSS offers. Strong fundamentals-driven philosophy, low portfolio turnover.

| Metric | Details |

| Fund Category | ELSS / Tax Saver |

| 5-Year Return | Approx 15-18% CAGR |

| ELSS Expense Ratio | ~0.6% direct plan |

| Portfolio Style | Value-oriented, Indian + international equity mix |

| Minimum SIP | Rs 500 per month |

| Risk Level | Moderate — international exposure adds currency risk |

| Best For | Investors wanting global diversification + tax saving in one fund |

4. DSP Tax Saver Fund

A well-diversified, balanced ELSS fund with a long track record. Consistent performer without extreme highs or lows. Mix of large and midcap stocks. Good for moderate-risk investors who want steady compounding without surprises.

| Metric | Details |

| Fund Category | ELSS / Tax Saver |

| 5-Year Return | Approx 14-17% CAGR |

| ELSS Expense Ratio | ~0.7% direct plan |

| Portfolio Style | Diversified large and midcap |

| Minimum SIP | Rs 500 per month |

| Best For | Moderate-risk investors, those wanting a balanced approach |

5. SBI Long Term Equity Fund

One of the oldest and largest ELSS funds in India — formerly known as SBI Magnum Tax Gain. More conservative approach with a large-cap tilt. Not the highest performer but offers stability and the comfort of being managed by the country’s largest public sector bank subsidiary. Good entry point for first-time equity investors.

| Metric | Details |

| Fund Category | ELSS / Tax Saver |

| 5-Year Return | Approx 13-16% CAGR |

| ELSS Expense Ratio | ~0.7% direct plan |

| Portfolio Style | Conservative, large-cap heavy |

| Minimum SIP | Rs 500 per month |

| Best For | Very conservative investors, those who prefer PSU-backed fund house |

ELSS Fund Comparison 2026 — Quick Reference

| Fund | Risk Level | Return Potential | Who Should Pick |

| Mirae Asset ELSS | Low-Medium | Good (16-18%) | Beginners, conservative equity investors |

| Quant Tax Plan | High | Very High (22%+) | Aggressive investors, 10+ year horizon |

| Parag Parikh Tax Saver | Medium | Good (15-18%) | Those wanting India + global exposure |

| DSP Tax Saver | Medium | Moderate (14-17%) | Balanced, steady-growth investors |

| SBI Long Term Equity | Low-Medium | Moderate (13-16%) | Conservative, PSU-fund-house preference |

ELSS SIP or Lumpsum — Which Is Better?

Both work for ELSS, but they behave differently due to the lock-in:

ELSS SIP: Each monthly instalment has its own 3-year lock-in from that date. So a 12-month SIP started today means the first instalment is redeemable after 3 years, but the last instalment is locked for 3 years from month 12. In practice this means full liquidity arrives over a rolling 12-month window from year 3 onwards.

ELSS Lumpsum: The entire investment is locked for exactly 3 years from the date of investment. Full amount becomes redeemable on one date. Simpler to track.

| For 80C planning: start an ELSS SIP of Rs 12,500 per month from April. By March you have invested Rs 1.5 lakh and used up your full 80C limit automatically — no last-minute scramble. ELSS SIP also benefits from rupee cost averaging over the year. |

ELSS Redemption Rules — What Happens After 3 Years

After the 3-year lock-in, ELSS units behave exactly like any other equity mutual fund — you can redeem fully, partially, or continue holding indefinitely. There is no obligation to redeem.

ELSS redemption rules on tax: gains from ELSS after 3 years are treated as Long Term Capital Gains (LTCG). The ELSS capital gains tax rate is 10% on gains above Rs 1.25 lakh per financial year. Below Rs 1.25 lakh — completely tax-free.

| Scenario | LTCG Tax Treatment |

| Total gain = Rs 80,000 in the year | Zero tax — below Rs 1.25 lakh threshold |

| Total gain = Rs 1,50,000 in the year | 10% on Rs 25,000 (excess above 1.25L) = Rs 2,500 tax |

| Total gain = Rs 3,00,000 in the year | 10% on Rs 1,75,000 = Rs 17,500 tax |

| Multiple ELSS funds — gains combined across all funds | Rs 1.25L threshold applies to total LTCG in the year |

| Tip: Smart ELSS redemption: if your LTCG is approaching Rs 1.25 lakh in a financial year, consider redeeming and reinvesting (tax harvesting) to reset your cost basis. This legally reduces your future LTCG tax burden. |

ELSS vs PPF 2026 — The Definitive Comparison

This is the most debated 80C choice in India. Here is the honest answer:

| Factor | ELSS | PPF |

| Lock-in period | 3 years | 15 years |

| Expected return | 12-16% CAGR (equity) | 7.1% (govt-fixed) |

| Return guarantee | No — market-linked | Yes — sovereign guarantee |

| Tax on gains | 10% LTCG above Rs 1.25L | Completely tax-free (EEE) |

| Liquidity after lock-in | Full — redeem anytime | Partial — limited withdrawals yr 7+ |

| Risk | Market risk present | Zero — government-backed |

| Best horizon | 7 years or more | 15 years (full term) |

| Best for | Wealth creation + tax | Safe savings + tax + retirement |

My view: For a 30-year-old with a 20-year investment horizon, ELSS will almost certainly create more wealth than PPF. For a 55-year-old looking for safe retirement savings, PPF is the right choice. For most working professionals, a combination works best — EPF plus ELSS to fill 80C, PPF for any additional safe allocation.

How to Invest in ELSS — Step by Step

- Open an account on Groww, Zerodha Coin, Kuvera, or any SEBI-registered platform

- Complete KYC — PAN plus Aadhaar plus bank account (one-time, 10 minutes)

- Search for your chosen ELSS fund — verify ‘Direct’ plan is selected

- Choose SIP (recommended) or lumpsum

- Set SIP date 3-5 days after your salary credit date

- Enable auto-debit mandate via UPI or net banking

- Do not redeem at 3 years unless you genuinely need the money — let it compound

| Tip: When you search for a fund, the name must contain ‘Direct’ to confirm you are in the direct plan. Example: ‘Mirae Asset ELSS Tax Saver Fund Direct Growth’ — not ‘Mirae Asset ELSS Tax Saver Fund Regular Growth’. The word Regular means you are paying distributor commission. |

Use our SIP Calculator to see how your ELSS investment grows over 5, 10, and 15 years — and Income Tax Calculator to check your 80C savings

Frequently Asked Questions

What is ELSS mutual fund and how does it work?

ELSS mutual fund meaning: Equity Linked Savings Scheme is a mutual fund that invests primarily in equity stocks and qualifies for Section 80C tax deduction up to Rs 1.5 lakh per year. It has the shortest lock-in period (3 years) among all 80C options. Returns are market-linked and historically 12-16% CAGR over 10+ years.

Can I invest more than Rs 1.5 lakh in ELSS?

Yes. The Rs 1.5 lakh limit is only for the 80C tax deduction. You can invest any amount in ELSS — amounts above Rs 1.5 lakh do not give additional 80C benefit but still grow and are subject to normal LTCG rules after the 3-year lock-in.

What happens to my ELSS SIP after the 3-year lock-in?

Each ELSS SIP instalment is unlocked 3 years from its investment date — not 3 years from when you started. After units unlock you can redeem, switch, or continue holding. Continuing to hold is usually the better choice if you do not need the money — equity rewards patience beyond the minimum 3-year period.

Is ELSS better than PPF for Section 80C in 2026?

For investors with a 7-plus year horizon who can handle equity volatility, ELSS has historically delivered significantly better returns than PPF. ELSS vs PPF 2026: ELSS wins on returns and liquidity (3-year lock-in vs 15-year). PPF wins on safety and tax-free maturity. Most financial advisors recommend using ELSS for the majority of your 80C limit and PPF for a smaller safe allocation.

How is ELSS taxed on redemption?

ELSS capital gains tax: gains after 3-year lock-in are Long Term Capital Gains (LTCG). LTCG up to Rs 1.25 lakh per financial year is completely tax-free. Gains above Rs 1.25 lakh are taxed at 10% without indexation. This is the lowest effective tax rate among all 80C investment options.

Which is the best ELSS fund for a first-time investor in 2026?

Mirae Asset ELSS Tax Saver Fund or DSP Tax Saver Fund are generally good starting points — both have consistent long-term track records, reasonable expense ratios in direct plan, and less volatility than aggressive funds like Quant Tax Plan. Start with one fund, not multiple, and invest via SIP.