Raju resigned from his job in January. He had Rs 3.8 lakh in his EPF account — money he and his employer had contributed over 4 years. He went to the EPFO office in Hyderabad with printed forms and supporting documents. He waited 3 hours. Was told his UAN was not linked to Aadhaar. Came back the next week with a fresh form. Was then told his bank account was not verified. A month later his claim was still pending.

His colleague Meena did the entire thing from her phone in 18 minutes. Money arrived in her account in 5 working days.

The difference: Meena had activated her UAN, linked Aadhaar, and verified her bank account — all before she even needed to withdraw. Raju had not.

This guide is your complete roadmap to EPF withdrawal in 2026 — online, fast, and without rejection.

Before You Start — 3 Prerequisites That Decide Everything

EPF withdrawal online is only possible if all three of these are in order. If any one is missing, your claim will be rejected or you will be forced to visit the EPFO office physically.

| Prerequisite | How to Check | How to Fix If Missing |

| UAN (Universal Account Number) is activated | Try logging in at unifiedportal-mem.epfindia.gov.in | Get UAN from employer. Activate at EPFO member portal using UAN + mobile number + Aadhaar OTP |

| Aadhaar linked and verified with UAN | Login to EPFO portal > Manage > KYC — check Aadhaar status | Add Aadhaar under KYC section. Employer must approve it. Takes 2-7 days. |

| Bank account verified (IFSC + account number) | Login > Manage > KYC — check bank account status shows Verified | Add bank under KYC > employer approves > EPFO digitally verifies. Takes 3-7 days. |

| Tip: Check all three prerequisites NOW — even if you are not planning to withdraw soon. Aadhaar and bank linking take 5-10 days with employer approval. You do not want to discover this gap the week you need the money. |

Types of EPF Withdrawal — Which One Do You Need?

| Type | When to Use | Form Required | Key Condition |

| Full Withdrawal (Final Settlement) | Left job, not joining another employer within 2 months | Form 19 (EPF) + Form 10C (EPS) | Must be unemployed for 2+ months |

| Partial Withdrawal (PF Advance) | Medical emergency, home loan, education, marriage — still employed | Form 31 | Varies by reason — see table below |

| Pension Withdrawal (EPS only) | Left job, less than 10 years service, want EPS refund | Form 10C | Service less than 10 years |

| Transfer to New Employer | Joining a new job — do not withdraw, transfer instead | Form 13 (online) | Recommended over withdrawal for tax |

| Warning: Do NOT withdraw EPF if you are joining a new employer within 2 months. Transfer it using Form 13 instead. Withdrawing and reinvesting means losing years of compound interest history. EPF at 8.25% guaranteed is one of the best debt instruments in India — keep it running. |

EPF Partial Withdrawal Rules — PF Advance 2026

If you are still employed and need money urgently, EPF partial withdrawal (called PF advance) is available for specific reasons. Each reason has its own eligibility conditions and limits:

| Reason | Service Required | Max Amount | Documents Needed |

| Medical emergency (self or family) | No minimum | 6x monthly wages OR employee share + interest (whichever lower) | Hospital certificate / medical bills |

| Marriage (self, sibling, child) | 7 years service | 50% of employee contribution | Marriage invitation / certificate |

| Higher education (self or child) | 7 years service | 50% of employee contribution | Admission letter from institution |

| Home loan repayment | 3 years service | Up to 90% of total EPF balance | Home loan account statement |

| Home purchase or construction | 5 years service | Up to 24x monthly wages | Property documents |

| Home renovation | 5 years service | Up to 12x monthly wages | Renovation estimate from contractor |

| Pre-retirement (age 54+) | Within 1 yr of retirement | Up to 90% of total balance | No documents required |

| Physically handicapped equipment | No minimum | 6x monthly wages | Doctor certificate for disability |

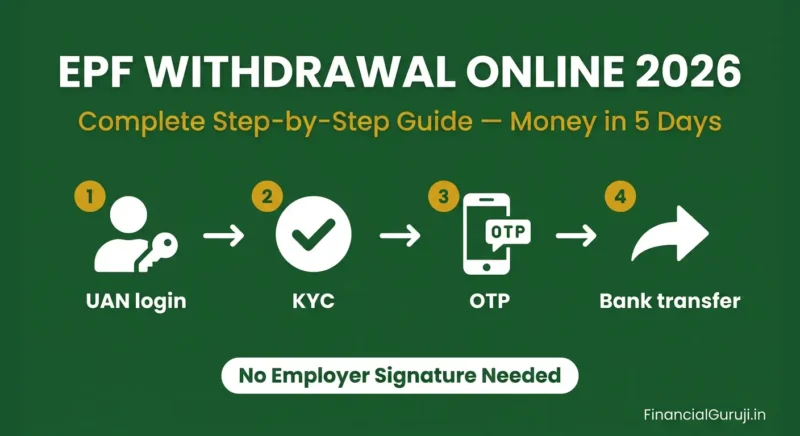

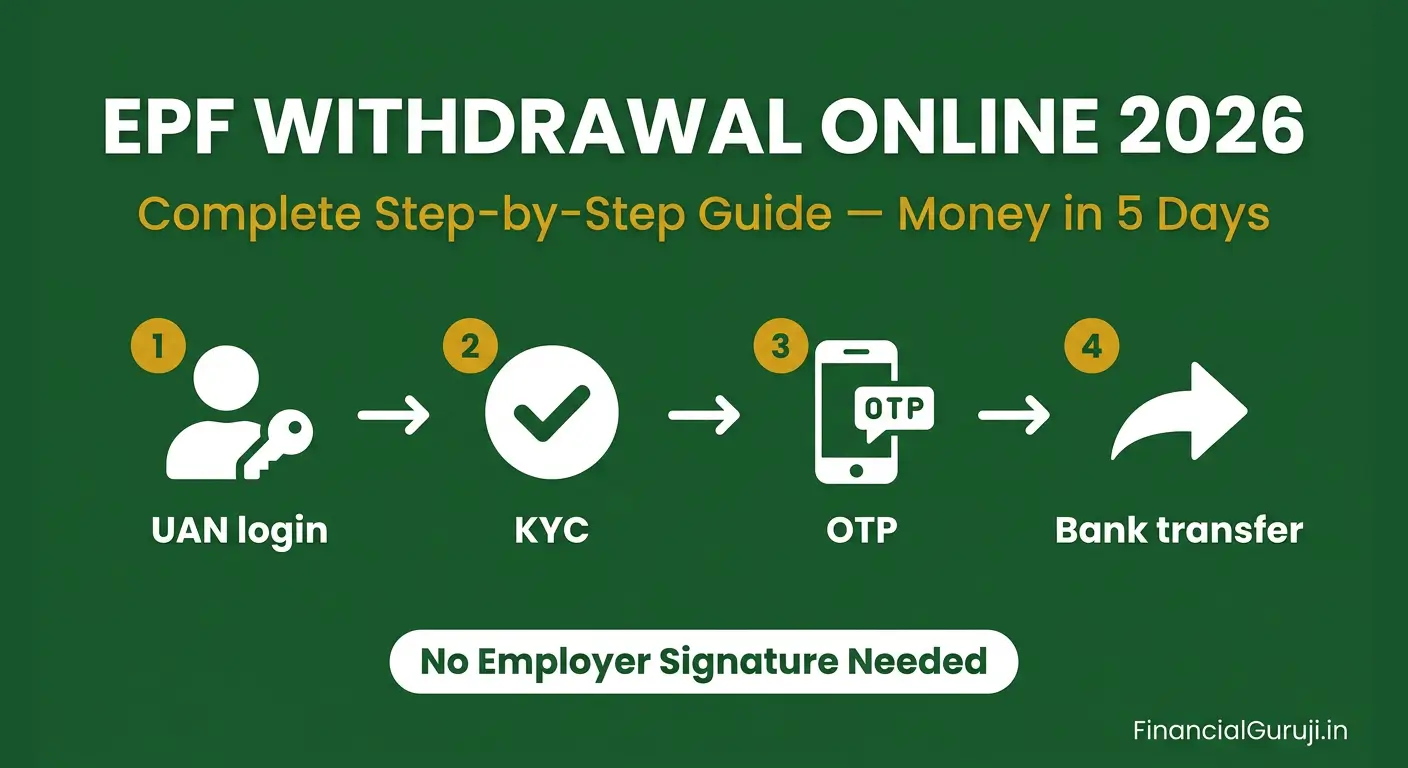

Full EPF Withdrawal — Step-by-Step Process Online

This is for full final settlement — when you have left a job and been unemployed for 2 or more months:

- Go to unifiedportal-mem.epfindia.gov.in and login with your UAN and password

- Click Online Services in the top menu, then select Claim (Form 31, 19, 10C, 10D)

- Your member details appear — verify name, Aadhaar, bank account. If anything looks wrong, stop and fix it first under Manage > KYC

- Click Proceed for Online Claim

- Select the claim type from the dropdown — Full EPF Settlement (Form 19) for your EPF balance, or Form 10C for pension withdrawal

- Enter your address as it appears in EPFO records

- Upload a cheque or bank passbook image (JPG or PDF, under 1 MB) as bank proof

- Enter the last 4 digits of your Aadhaar for verification

- Check the Terms and Conditions box and click Get Aadhaar OTP

- Enter the OTP received on your Aadhaar-linked mobile number

- Click Submit Claim Form

| After submission: claim reference number appears. EPF withdrawal time limit per EPFO guidelines is 3 working days. In practice, 5-7 working days is typical. Check claim status under Online Services > Track Claim Status using your UAN. |

EPF Claim Status Check — How to Track

After submitting your EPF withdrawal claim, track it using the EPFO member portal:

- Login to EPFO portal > Online Services > Track Claim Status

- Enter your UAN — status updates in real time

- Status stages: Claim Submitted > Under Process > Claim Settled > NEFT Initiated > Amount Credited

- SMS alert is sent to your Aadhaar-registered mobile at each stage

- If status shows Rejected — reason is visible. Fix the issue and resubmit.

| Tip: EPF claim status can also be checked by missed call to 011-22901406 from your UAN-registered mobile number. You get an SMS with balance and last contribution details. For claim status only: call EPFO toll-free 1800-118-005. |

Common EPF Withdrawal Rejected Reasons — and How to Fix Them

These are the most frequent reasons why EPF withdrawal claims get rejected:

| Rejection Reason | Root Cause | Fix Required | Time to Resolve |

| Name mismatch between EPFO and Aadhaar | Name spelling differs (e.g. ‘Raju’ vs ‘Raju Kumar’) | Update name in EPFO via employer or EPFO Grievance portal | 7-15 days |

| Bank account not verified | Bank KYC not approved by employer | Request employer to approve bank KYC in employer portal | 3-7 days |

| Aadhaar mobile number mismatch | OTP not coming because Aadhaar has old mobile number | Update mobile in Aadhaar at uidai.gov.in or Aadhaar Seva Kendra | 7-15 days |

| Date of joining or leaving mismatch | Employer entered wrong dates in ECR | Employer must correct in EPFO employer portal | 5-10 days |

| Claim submitted before 2-month wait | Submitted immediately after resignation | Wait 2 full months from last working day, resubmit | Wait period only |

| KYC documents unclear | Uploaded image is blurry or wrong file | Re-upload clear JPG/PDF under 1 MB | Immediate resubmit |

| Service record discrepancy | Multiple UAN accounts for same employee | Merge UANs via EPFO portal or employer HR | 15-30 days |

For issues that require employer action, raise a grievance on epfigms.gov.in — the EPFO grievance portal. Grievances are resolved within 15-30 days and you get a reference number to track progress.

EPF Withdrawal Tax Rules — Very Important

The tax treatment of EPF withdrawal depends entirely on how long you have been in continuous service:

| Service Duration | EPF Tax Treatment | TDS Deducted? | Action Required |

| 5 years or more (continuous) | Completely tax-free — no tax on withdrawal | No TDS | Nothing — enjoy full amount tax-free |

| Less than 5 years — above Rs 50K | Taxable as income in year of withdrawal. Added to salary income | TDS at 10% | Submit Form 15G (below 60) or 15H (senior citizen) to avoid TDS if income below taxable limit |

| Less than 5 years — below Rs 50K | Taxable but no TDS deducted | No TDS | Declare in ITR — add to other income and pay tax accordingly |

| Service broken by job change | 5 years counted across employers if EPF transferred (Form 13) | Depends on total | Always transfer EPF when changing jobs — do not withdraw |

Use our free Income Tax Calculator to check how much tax you will pay after EPF withdrawal → Income Tax Calculator

| Warning: EPF withdrawal before 5 years tax trap: If you withdraw before 5 years of continuous service, not only is the withdrawal taxable — the employer’s contribution and interest on both portions become taxable. The tax hit can be 20-30% of your corpus. Transfer, do not withdraw, when changing jobs. |

EPF Pension Withdrawal — EPS Amount

Your EPF account actually has two parts that many people do not know about:

- EPF account: Employee contribution (12% of Basic) + Employer contribution (3.67% of Basic) — this is the main balance

- EPS (Employee Pension Scheme): Employer contributes 8.33% of Basic to this — maximum Rs 1,250 per month — separate from EPF balance

EPF pension withdrawal via Form 10C: If your service is less than 10 years, you can withdraw the EPS accumulation as a lump sum. If service is 10+ years, you cannot withdraw EPS — it converts to monthly pension from age 58.

For most people below 10 years of service, the EPS balance is small (capped at Rs 1,250 employer contribution per month). But it is worth claiming — do not leave it behind.

EPF Transfer vs Withdrawal — When to Choose What

| Situation | Recommended Action | Reason |

| Joining new employer within 2 months | Transfer via Form 13 online | Preserves 5-year continuity for tax exemption. EPF compound interest continues at 8.25%. |

| Unemployed for 2+ months, need funds | Full withdrawal Form 19 + 10C | Legitimate use case. Check if 5-year condition met for tax-free exit. |

| Unemployed but do not need funds now | Leave it — no rush | EPF earns 8.25% guaranteed even after resignation. Withdraw when you actually need it. |

| Starting own business | Partial withdrawal if needed | Use PF advance for specific needs. Keep rest earning 8.25%. |

| Moving abroad permanently | Full withdrawal after 2 months | Non-residents can withdraw fully. No TDS if 5+ years service. |

Use our EPF Calculator to know your current EPF corpus and projected balance at retirement — then decide whether to withdraw or let it grow

EPFO Official Site — epfindia.gov.in

Frequently Asked Questions

How long does EPF withdrawal take in 2026?

The official EPF withdrawal time limit is 3 working days per EPFO guidelines. In practice, online claims settle in 5-7 working days if all KYC is in order. Offline claims (physical forms at EPFO office) can take 15-30 days. Online is always faster — use the EPFO member portal.

Can I withdraw EPF without employer signature in 2026?

Yes — this is the key advantage of the online EPF withdrawal process. If your UAN is activated with verified Aadhaar and bank account, employer signature is NOT required. The Aadhaar OTP replaces the employer attestation completely. This is why the UAN-Aadhaar linking is so important.

What is Form 15G for EPF withdrawal?

Form 15G is a self-declaration that your total income is below the taxable limit. You submit it to EPFO to prevent TDS deduction on EPF withdrawal when your service is less than 5 years and the withdrawal amount is above Rs 50,000. If your income is above Rs 5 lakh (taxable), you cannot use Form 15G — pay the applicable tax instead.

My EPF claim is showing Under Process for 15 days. What to do?

First, check if there is any rejection reason visible in the portal — sometimes it shows rejected without SMS notification. If genuinely stuck under process, raise a grievance on epfigms.gov.in with your UAN, claim reference number, and a brief description. EPFO resolves most grievances within 15 working days.

I have multiple UAN numbers from different jobs. How to merge?

Multiple UANs cause EPF withdrawal rejected status and also break the 5-year continuity count. To merge: login to EPFO portal > One Member One EPF Account > enter details of the UANs to merge. Alternatively, contact your current employer’s HR who can initiate the merge through the employer portal. This is a common issue — get it resolved before you need to withdraw.

Can I withdraw EPF to pay off home loan EMIs?

Yes — EPF partial withdrawal for home loan repayment is allowed after 3 years of service. You can withdraw up to 90% of your total EPF balance for this purpose. Submit Form 31 online with your home loan account statement as supporting document. Note this is different from Section 24b tax deduction — both can be used simultaneously.