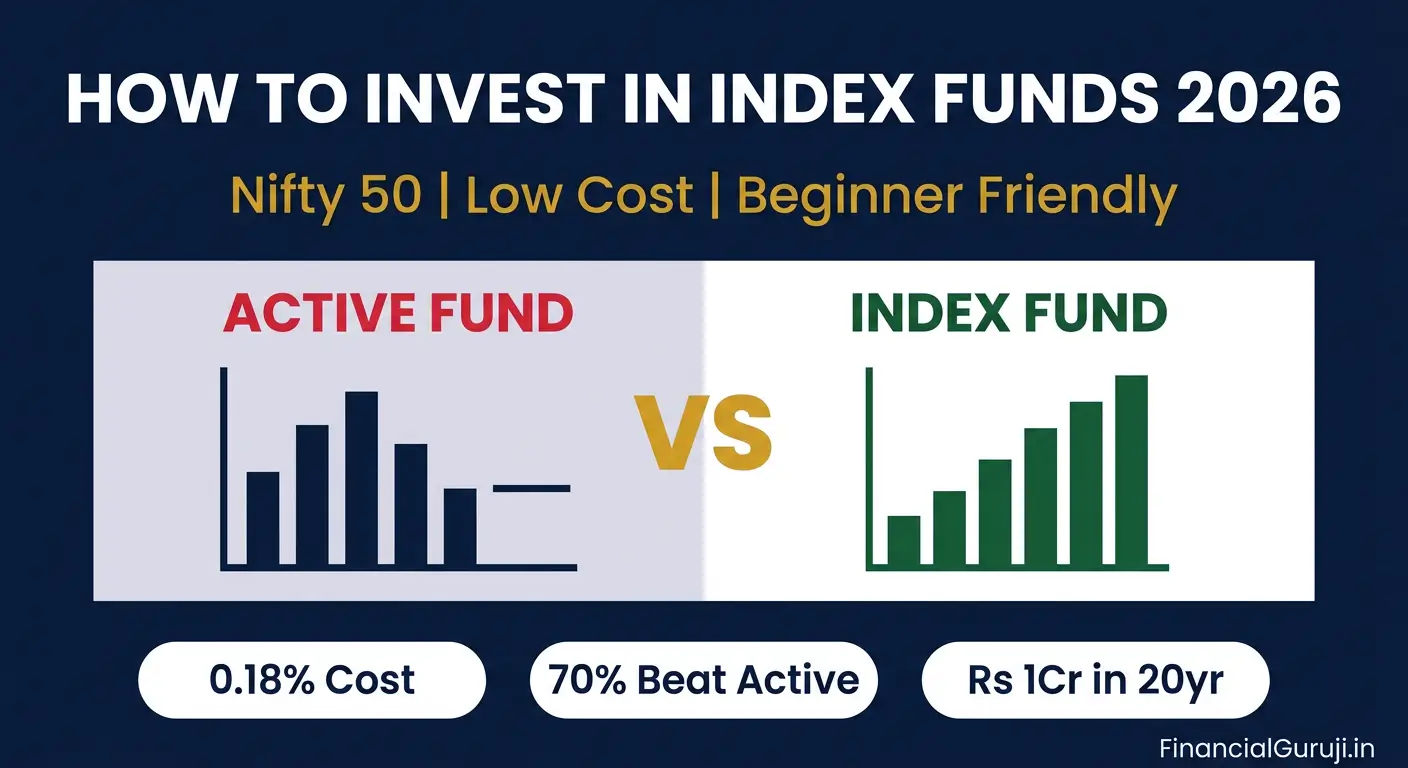

In 2023, SEBI published data showing that over a 10-year period, more than 70% of large-cap active mutual funds in India failed to beat their benchmark index. Fund managers with teams of analysts, Bloomberg terminals, and years of experience — underperforming a simple index that just holds all the stocks in proportion.

The investors in those active funds paid 1.5% to 2.5% in expense ratio every year for this underperformance. The investors in index funds paid 0.1% to 0.2% and did better.

This is not a new story. It is why index funds have become the default recommendation for long-term investors across the world — and why they are rapidly gaining ground in India too.

Here is everything you need to know to start investing in index funds in India in 2026.

What Is an Index Fund — Index Fund Meaning India

An index fund is a mutual fund that simply replicates a stock market index. It buys all the stocks in the index in the same proportion as the index itself — nothing more, nothing less.

The Nifty 50 index fund, for example, holds all 50 stocks of the Nifty 50 index in the same weights as the index. When Reliance is 10% of Nifty 50, the fund holds 10% in Reliance. No fund manager is deciding what to buy or sell — the portfolio just mirrors the index automatically.

Because there is no active stock selection, the costs are dramatically lower. A typical active large-cap fund charges 1.5% to 2% expense ratio per year. A Nifty 50 index fund in direct plan charges 0.1% to 0.2%. On a Rs 10 lakh investment over 20 years, that cost difference compounds to Rs 4 to 6 lakh in extra wealth staying in your pocket.

Index Fund vs Active Fund — The Numbers for India

| Comparison Factor | Index Fund | Active Mutual Fund |

| How it works | Mirrors index automatically | Fund manager picks stocks |

| Expense ratio (direct) | 0.1% to 0.25% | 0.5% to 1.8% |

| Fund manager risk | None — no human decisions | Manager change affects performance |

| 10-year performance | Matches index returns (12-13% CAGR) | 70% underperform index after costs |

| Transparency | 100% — you know every stock held | Disclosed monthly with delay |

| Minimum SIP | Rs 100 to Rs 500 depending on platform | Rs 500 to Rs 1000 typically |

| Best for | Long-term wealth, passive investors | Short-term tactical bets, midcap/smallcap |

| Index funds do not always win. In midcap and smallcap categories, skilled active fund managers do add value — the active vs passive debate is clearest in large-cap where information is widely available and markets are efficient. For your large-cap allocation, index funds are the default right answer. |

Which Index Fund to Choose — The Main Options in India

1. Nifty 50 Index Fund — The Foundation

The Nifty 50 tracks India’s 50 largest companies by market capitalisation — Reliance, TCS, HDFC Bank, Infosys, ICICI Bank and 45 others. This is the most liquid, most researched, and most replicated index in India.

Best for: Core long-term equity portfolio. Every Indian equity investor should have Nifty 50 as the base.

Top Nifty 50 index funds by expense ratio (direct plan):

- UTI Nifty 50 Index Fund Direct — 0.18% expense ratio, large AUM, very low tracking error

- HDFC Index Fund Nifty 50 Plan Direct — 0.20% expense ratio, reliable tracking

- SBI Nifty Index Fund Direct — 0.20% expense ratio, PSU-backed fund house

- Nippon India Index Fund Nifty 50 Direct — 0.20% expense ratio

| Tip: Tracking error is as important as expense ratio for index funds. It measures how closely the fund actually follows its index. Lower tracking error = better replication. UTI Nifty 50 and HDFC Index Fund consistently show among the lowest tracking errors in this category. |

2. Nifty Next 50 Index Fund — The Growth Accelerator

The Nifty Next 50 tracks ranks 51 to 100 in market cap — the companies just below the top 50. Many Nifty 50 companies started in Nifty Next 50 and graduated up. This index has historically given higher returns than Nifty 50 with somewhat higher volatility.

Nifty Next 50 index fund is ideal for investors who want more growth potential than pure large-cap but with more stability than midcap funds.

- UTI Nifty Next 50 Index Fund Direct — 0.30% expense ratio

- HDFC Nifty Next 50 Index Fund Direct — 0.32% expense ratio

3. Sensex Index Fund — NSE vs BSE

The Sensex index fund tracks the BSE Sensex — India’s oldest index with 30 large-cap stocks. Performance is very similar to Nifty 50 since both track large Indian companies, with significant overlap in top holdings.

No strong reason to pick Sensex over Nifty 50 or vice versa for most investors — both are fine. If your broker or platform offers only one, go with what is available.

4. Nifty 500 or Total Market Index Fund

The broadest index fund option — tracks 500 companies across large, mid, and small caps. Gives exposure to the entire Indian market in one fund. Ideal for investors who want a single-fund equity portfolio.

- UTI Nifty 500 Index Fund Direct — 0.32% expense ratio

- Motilal Oswal Nifty 500 Index Fund Direct — 0.35% expense ratio

Best Index Funds India 2026 — Quick Comparison

| Fund | Index Tracked | Expense Ratio | 5-Year Return | Best For |

| UTI Nifty 50 Index Fund Direct | Nifty 50 | 0.18% | ~14-16% CAGR | Core large-cap, beginners |

| HDFC Index Fund Nifty 50 Direct | Nifty 50 | 0.20% | ~14-16% CAGR | Core large-cap |

| UTI Nifty Next 50 Index Fund Direct | Nifty Next 50 | 0.30% | ~15-18% CAGR | Growth, medium risk |

| Motilal Oswal Nifty 500 Index Direct | Nifty 500 | 0.35% | ~14-17% CAGR | Whole market exposure |

| SBI Nifty Index Fund Direct | Nifty 50 | 0.20% | ~14-16% CAGR | PSU-preferred investors |

Note: Returns shown are approximate historical CAGR. All index funds tracking the same index will have very similar returns — the differentiator is expense ratio and tracking error, not fund manager skill.

Index Fund Returns India — 10 Year Perspective

The most important thing to understand about index fund returns: they follow the market. In good years the index goes up strongly. In bad years it falls. What matters is the long-term compound return.

| Time Period | Nifty 50 Approximate CAGR | Rs 10,000/month SIP Result |

| 1 year | Highly variable, -20% to +40% | Not meaningful — too short |

| 3 years | 12-18% CAGR (recent data) | ~Rs 4.5 to 5 lakh from Rs 3.6L invested |

| 5 years | 13-16% CAGR | ~Rs 9 to 10 lakh from Rs 6L invested |

| 10 years | 12-14% CAGR (historical avg) | ~Rs 23 to 27 lakh from Rs 12L invested |

| 20 years | ~13% CAGR (long-term avg) | ~Rs 1 crore+ from Rs 24L invested |

| The index fund returns India story is simple: give it time. A Rs 10,000 SIP in Nifty 50 for 20 years at 13% CAGR grows to over Rs 1 crore. The same Rs 10,000 in a savings account at 3.5% grows to Rs 34 lakh. Patience plus low cost is the entire strategy. |

How to Start an Index Fund SIP — Step by Step

- Choose a platform: Groww, Zerodha Coin, Kuvera, or Paytm Money are the most popular. All offer direct plans.

- Complete KYC: PAN card + Aadhaar + bank account. One-time process, takes 10-15 minutes online.

- Search for your chosen index fund — type ‘UTI Nifty 50 Index Fund Direct Growth’ and verify the word ‘Direct’ is in the name.

- Select SIP option — choose monthly frequency.

- Set SIP amount — minimum Rs 500 for most platforms, no maximum.

- Choose SIP date — 3 to 5 days after your salary credit date so funds are always available.

- Set up auto-debit mandate via net banking or UPI — one-time setup.

- That is it. SIP runs automatically every month. Check performance quarterly, not daily.

| Tip: Direct plan vs regular plan: Always search for and select ‘Direct’ in the fund name. Regular plans include distributor commission (0.8 to 1.5% extra cost per year) and are sold through brokers and banks. Direct plans cut out the middleman. Same fund, same index, dramatically different long-term outcome. |

Index Fund SIP — How Much to Invest

Use the 50-30-20 rule as a starting point: 50% expenses, 30% lifestyle, 20% investments. Of your investment amount, put at least 60% in equity index funds if your horizon is 7+ years.

| Monthly Salary | Suggested SIP in Index Fund | 20-Year Projected Corpus (13% CAGR) |

| Rs 30,000 | Rs 3,000/month | ~Rs 30 lakh |

| Rs 50,000 | Rs 7,500/month | ~Rs 75 lakh |

| Rs 75,000 | Rs 12,000/month | ~Rs 1.2 crore |

| Rs 1,00,000 | Rs 20,000/month | ~Rs 2 crore |

| Rs 1,50,000 | Rs 30,000/month | ~Rs 3 crore |

Use the SIP Calculator on this site to run your own numbers — change the assumed return and time horizon to see different scenarios.

Common Mistakes to Avoid With Index Funds

- Stopping SIP during market falls — this is exactly when you should be buying more units at lower prices. Market corrections are on sale events for SIP investors.

- Investing in too many index funds — two Nifty 50 funds from different AMCs is not diversification. It is duplication. One Nifty 50 fund is sufficient for large-cap exposure.

- Checking returns daily or weekly — index fund investing is a 7 to 20 year game. Checking daily creates anxiety and encourages bad decisions.

- Choosing regular plan over direct — this single mistake costs lakhs over 10-20 years. Always verify ‘Direct’ in the fund name.

- Confusing index funds with ETFs — index funds and ETFs (Exchange Traded Funds) both track an index but ETFs trade on stock exchanges like shares. For SIP investors, index funds (not ETFs) are easier to use as they can be set up with automatic monthly debit.

Passive Investing India — Is It Right for You?

Passive investing through index funds suits you if:

- You have a 7-year or longer investment horizon

- You do not want to research individual stocks or track fund manager performance

- You want low cost — every rupee saved in expense ratio compounds over decades

- You understand that short-term market falls are normal and will not panic-sell

Active funds may be better if you want exposure to midcap or smallcap categories where skilled managers do add value, or if you have specific tactical views on market sectors. For most salaried investors building long-term wealth — index funds for large-cap, active funds for midcap/smallcap, and debt funds for stability — is the practical balanced approach.

Use our SIP Calculator — enter your monthly amount and see your index fund corpus at 10, 15, and 20 years

Frequently Asked Questions

What is the minimum amount to invest in an index fund in India?

Most platforms allow index fund SIP starting at Rs 100 to Rs 500 per month. Lumpsum minimum is typically Rs 1,000 to Rs 5,000 depending on the AMC. There is no maximum investment limit. You can start with Rs 500 and increase over time.

Is Nifty 50 index fund safe for beginners in 2026?

Index funds carry equity market risk — they fall when markets fall. However, for a 10+ year horizon, Nifty 50 index funds are among the most reliable equity investment options for beginners. The key is staying invested through market cycles. For money needed within 3 years, use debt instruments instead.

UTI Nifty 50 vs HDFC Index Fund — which is better?

Both are excellent. UTI Nifty 50 has a slightly lower expense ratio (0.18% vs 0.20%) and has historically shown very low tracking error. HDFC Index Fund is also well-managed. The difference in returns over 10 years is minimal. Choose the one available on your preferred platform and do not overthink it.

Can I invest in index funds through SIP?

Yes — index fund SIP is the recommended way to invest. Monthly SIP gives you rupee cost averaging — you buy more units when markets are low and fewer when markets are high. This naturally reduces your average cost over time and removes the need to time the market.

How are index fund gains taxed in India?

Index funds are equity mutual funds for tax purposes. Gains held less than 1 year: Short Term Capital Gains (STCG) taxed at 20%. Gains held more than 1 year: Long Term Capital Gains (LTCG) above Rs 1.25 lakh per year taxed at 12.5%. For long-term SIP investors, most gains fall in the LTCG category.

What is expense ratio in index fund and why does it matter?

Expense ratio is the annual fee the AMC charges to manage the fund — deducted from the fund’s NAV daily. A total expense ratio index fund of 0.18% means Rs 180 per year on Rs 1 lakh invested. On an active fund at 1.8%, you pay Rs 1,800 per year. Over 20 years on a growing corpus, this Rs 1,620 annual difference compounds to lakhs.