Venkatarao retired from his government job in Vijayawada in 2024 with a gratuity and provident fund corpus of Rs 28 lakh. His children suggested mutual funds. His bank relationship manager pitched ULIPs. His neighbour told him about a new stock that was going up.

Venkatarao wanted none of that. He had spent 30 years in a government job — steady income, zero surprises. He wanted the same in retirement. He wanted money in his account every month without touching the principal.

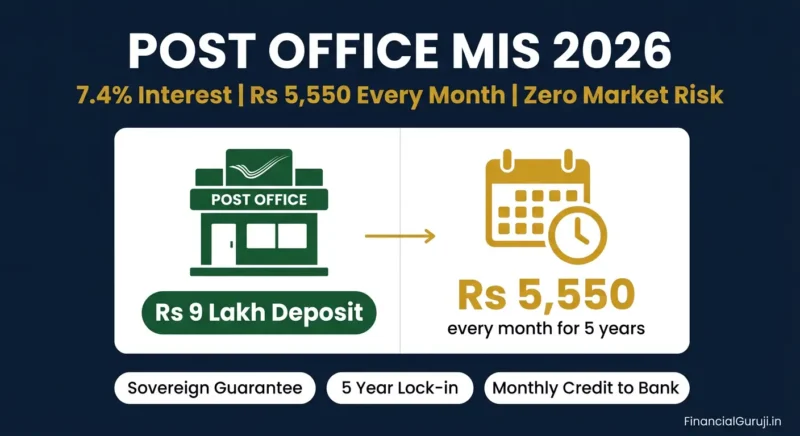

He put Rs 9 lakh in Post Office MIS. Every month since then, Rs 5,550 arrives in his savings account — on the same date, without fail. The remaining Rs 19 lakh went to SCSS (Senior Citizen Savings Scheme). Between the two, his monthly income is Rs 18,000 — no market risk, no fund manager decisions, no sleepless nights.

That is what Post Office MIS is for. Here is everything you need to know.

What is Post Office MIS — POMIS

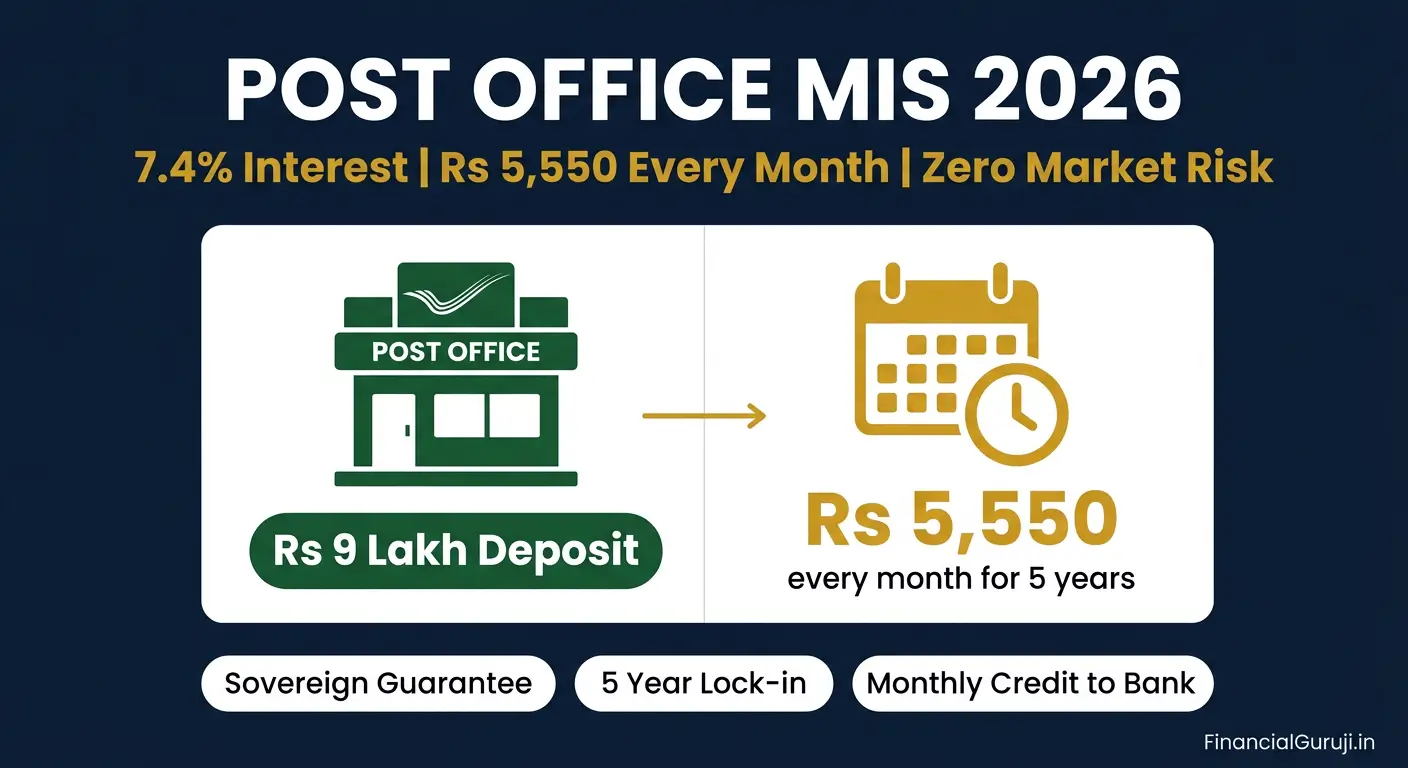

Post Office Monthly Income Scheme (POMIS or MIS) is a savings scheme offered by India Post that pays a fixed monthly interest on a lump sum deposit. It is backed by the Government of India — the same sovereign guarantee as PPF and SSY.

The key feature: interest is paid every month directly to your linked savings account. The principal stays intact for the full 5-year tenure and is returned at maturity. It is essentially a government-guaranteed fixed income instrument — like an FD that pays monthly interest instead of at maturity.

Post Office MIS Interest Rate 2026 — Current and Historical

| Period | POMIS Interest Rate | Monthly Payout on Rs 9L |

| FY 2020-21 | 6.6% | Rs 4,950/month |

| FY 2022-23 | 6.7% | Rs 5,025/month |

| FY 2023-24 | 7.4% | Rs 5,550/month |

| FY 2024-25 | 7.4% | Rs 5,550/month |

| Q1 FY 2026-27 (Apr 2026) | 7.4% | Rs 5,550/month — check NSIA for latest |

| POMIS interest rate of 7.4% is guaranteed for the full 5-year tenure from the date of account opening — it does not change quarterly like SSY or PPF. Whatever rate applies when you open the account locks in for 5 years. This rate certainty is a major advantage for income planning. |

Post Office MIS — Key Features 2026

| Feature | Details |

| Current interest rate | 7.4% per annum — paid monthly |

| Tenure | 5 years — fixed, no extension option (only renewal) |

| Minimum deposit | Rs 1,000 |

| Maximum deposit — single | Rs 9,00,000 (Rs 9 lakh) |

| Maximum deposit — joint | Rs 15,00,000 (Rs 15 lakh) — equally shared among holders |

| Number of accounts | Multiple accounts allowed — but total across all accounts cannot exceed Rs 9L (single) or Rs 15L (joint) |

| Who can open | Any Indian resident individual above 10 years. NRIs cannot open POMIS. |

| Joint account holders | Maximum 3 adults — joint A or joint B basis |

| Payout | Monthly interest credited to linked post office savings account or bank account via ECS |

| Nomination | Available — nominee receives principal + any unclaimed interest on death |

| Premature withdrawal | Allowed after 1 year with penalty (see below) |

| Tax on interest | Taxable — added to income, taxed at slab rate. No TDS below Rs 40,000/year. |

| 80C benefit | No — POMIS investment does not qualify for Section 80C |

Monthly Income — How Much Will You Receive

| Investment Amount | Monthly Interest (7.4%) | Annual Income | 5-Year Total Income |

| Rs 1,00,000 | Rs 617/month | Rs 7,400 | Rs 37,000 |

| Rs 2,00,000 | Rs 1,233/month | Rs 14,800 | Rs 74,000 |

| Rs 5,00,000 | Rs 3,083/month | Rs 37,000 | Rs 1,85,000 |

| Rs 9,00,000 | Rs 5,550/month | Rs 66,600 | Rs 3,33,000 |

| Rs 15,00,000 | Rs 9,250/month | Rs 1,11,000 | Rs 5,55,000 (joint account) |

Maximum single account: Rs 9 lakh generates Rs 5,550 per month for 5 years — and your Rs 9 lakh principal is returned in full at maturity. Joint account maximum Rs 15 lakh generates Rs 9,250 per month.

| Tip: Couple strategy: husband opens single POMIS Rs 9L + wife opens single POMIS Rs 9L = combined Rs 18L invested, Rs 11,100/month combined income. This is fully within individual limits and completely legal. No joint account needed — two separate single accounts. |

POMIS Premature Withdrawal Rules

POMIS allows premature withdrawal after 1 year with a penalty on principal:

| Withdrawal Timing | Penalty on Principal | Net Amount Received |

| Before 1 year | Not allowed | Cannot withdraw |

| After 1 year, before 3 years | 2% deducted from principal | Rs 9L deposit → Rs 8,82,000 returned |

| After 3 years, before 5 years | 1% deducted from principal | Rs 9L deposit → Rs 8,91,000 returned |

| At 5-year maturity | No penalty | Full Rs 9,00,000 returned |

| Warning: Do not invest emergency funds in POMIS. The 1-2% principal deduction on early withdrawal means you lose Rs 9,000 to Rs 18,000 on a Rs 9 lakh investment. Keep 6 months expenses in a liquid savings account or liquid mutual fund before investing in POMIS. |

POMIS Renewal Rules — What Happens at Maturity

At 5-year maturity, Post Office MIS does NOT auto-renew. You have two options:

- Withdraw the principal and close the account — full Rs 9 lakh returned

- Reinvest by opening a fresh 5-year POMIS account — at the new prevailing interest rate

There is a 2-year window after maturity during which the principal earns Post Office savings account rate (currently 4%) instead of MIS rate. After 2 years of inaction, the account is treated as matured and closed.

Smart strategy at maturity: if POMIS rates are good, reinvest. If rates have fallen, consider SCSS (for senior citizens) or bank FD with quarterly payout instead.

Post Office MIS Tax Treatment

This is the most important thing to understand about POMIS before investing:

- Monthly interest from POMIS is fully taxable — added to your total income and taxed at your applicable income tax slab rate

- No TDS is deducted if annual interest is below Rs 40,000 (Rs 50,000 for senior citizens) — but you must declare it in ITR regardless

- If annual interest exceeds Rs 40,000 — TDS at 10% is deducted by the post office

- There is NO Section 80C benefit on POMIS investment — the deposit itself does not reduce your taxable income

- At maturity, only the principal is returned — no tax on principal since it was already your own money (post-tax)

| POMIS tax reality for different brackets: At 7.4% interest on Rs 9 lakh = Rs 66,600/year gross interest. In 30% slab: Rs 19,980 tax, net income Rs 46,620, effective post-tax yield = 5.18%. In 0% slab (income below Rs 7L new regime): full Rs 66,600, effective yield = 7.4%. POMIS is most efficient for people with zero or low income — retirees, homemakers, parents investing for non-earning children. |

Post Office MIS vs Bank FD — Comparison

| Factor | Post Office MIS | Bank FD (5-year) |

| Interest rate | 7.4% (locked for 5 years) | 6.5% to 7.5% (varies by bank) |

| Payout frequency | Monthly — credited to account | Quarterly or at maturity |

| Principal safety | Sovereign guarantee | DICGC insured up to Rs 5 lakh per bank |

| Maximum safe amount | Rs 9L single / Rs 15L joint | Rs 5 lakh DICGC limit per bank |

| Premature withdrawal | After 1 year, 1-2% penalty | Penalty varies — 0.5% to 1% typically |

| 80C benefit | No | Yes — 5-year tax saver FD only |

| Tax on interest | Taxable at slab rate | Taxable at slab rate — TDS at 10% |

| Nomination | Yes | Yes |

| Best for | Monthly income, retirement | Lump sum parking, 80C saving |

For amounts above Rs 5 lakh, Post Office MIS is safer than bank FD due to sovereign guarantee. For Rs 5 lakh and below, a good bank FD offering 7.5% is comparable to POMIS at 7.4% — choose based on payout frequency preference and convenience.

Who Should Invest in Post Office MIS

| Investor Profile | Suitable? | Reason |

| Retirees needing monthly income | Excellent fit | Guaranteed monthly payout, zero market risk, sovereign safety |

| Homemakers with lump sum to deploy | Good fit | Monthly income for household expenses, no market exposure |

| Senior citizens (also consider SCSS) | Good fit | SCSS rate is 8.2% — higher than POMIS. Use both for income diversification |

| Salaried in 30% tax slab | Poor fit | After tax, effective yield is 5.18% — bank FD or debt fund more efficient |

| Young investors (25-40 years) | Not recommended | Better to invest in equity for long-term wealth. POMIS is not a growth instrument |

| Parents investing for minor children | Acceptable | Minor account allowed — but consider SSY if girl child, or equity SIP for longer horizon |

How to Open Post Office MIS Account — Documents Needed

- Visit your nearest post office — any branch across India

- Carry: Aadhaar card + PAN card + passport size photograph + cancelled cheque or bank passbook for ECS setup

- Fill Form 1 for MIS account opening — available at counter or download from India Post website

- Make deposit — cash or cheque or demand draft in favour of ‘Postmaster’

- Receive passbook — keep it safely for all future transactions including maturity withdrawal

- ECS setup: provide your bank account details for monthly interest credit — interest arrives by the 1st working day after deposit date each month

| Tip: Open POMIS account at your home post office for easiest access. If you move cities, POMIS account can be transferred to any post office in India free of charge — similar to SSY transfer rules. |

Post Office Savings Schemes 2026 — Complete Rate Comparison

POMIS is one of several Post Office savings schemes. Here is how all of them compare:

| Scheme | Rate | Tenure | Tax Benefit | Best For |

| Savings Account | 4.0% | Ongoing | None | Emergency fund |

| 1-Year TD | 6.9% | 1 year | None | Short-term parking |

| 2-Year TD | 7.0% | 2 years | None | Medium-term |

| 3-Year TD | 7.1% | 3 years | None | Medium-term |

| 5-Year TD | 7.5% | 5 years | 80C yes | Tax saving + FD |

| 5-Year RD | 6.7% | 5 years | None | Disciplined monthly saving |

| MIS (POMIS) | 7.4% | 5 years | None | Monthly income |

| Senior Citizen SS (SCSS) | 8.2% | 5+3 years | 80C yes | Senior citizens |

| PPF | 7.1% | 15 years | EEE (80C) | Long-term safe wealth |

| NSC | 7.7% | 5 years | 80C yes | Safe 5-year investment |

| Sukanya Samriddhi (SSY) | 8.2% | 21 years | EEE (80C) | Girl child education |

| KVP | 7.5% | ~9.7 yrs | None | Doubling money safely |

Use our Post Office Savings Calculator — compare POMIS, SCSS, and FD monthly income side by side for your investment amount