Three colleagues. Same salary — Rs 12 lakh per year. Same goal — retirement corpus. But three completely different choices for their Section 80C investment.

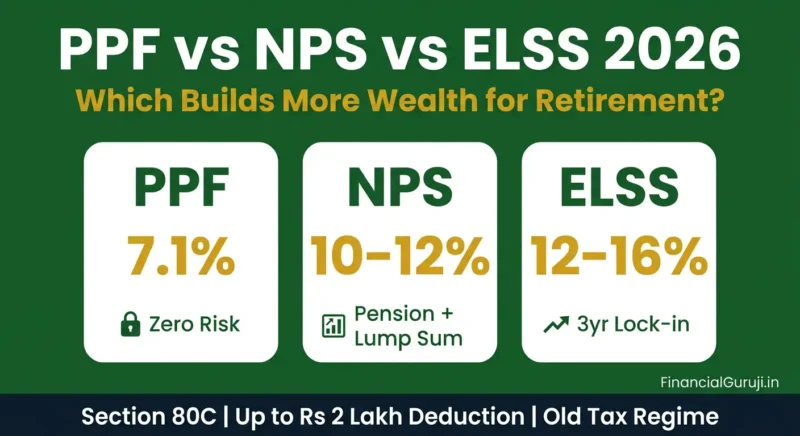

Anand puts Rs 1.5 lakh every year into PPF. Guaranteed 7.1%, completely tax-free, zero risk. Sleeps well at night.

Bhanu contributes Rs 1.5 lakh to NPS — 75% in equity, 25% in bonds. Market-linked returns, tax benefit on withdrawal, mandatory annuity at retirement. Thinks long-term.

Chandra invests Rs 1.5 lakh in ELSS mutual funds. Full equity exposure, shortest lock-in of the three, highest return potential, taxed on gains above Rs 1.25 lakh.

Thirty years later, the difference in their retirement corpus could be Rs 50 lakh to Rs 1.5 crore — from the same Rs 1.5 lakh annual investment. The choice matters enormously.

Here is the complete comparison to help you make the right one.

The Quick Verdict — Before the Details

| If You Are… | Best Choice | Why |

| Risk-averse, want guaranteed returns, fine with 15-year lock-in | PPF | Sovereign guarantee, EEE tax status, 7.1% guaranteed — nothing touches it for safety |

| Salaried, want retirement corpus, can lock money till age 60 | NPS | Extra Rs 50,000 deduction under 80CCD(1B), market-linked growth, employer can also contribute |

| Long-term investor (7+ years), want highest return, fine with equity risk | ELSS | Shortest lock-in (3 years), highest return potential (12-16%), only 10% LTCG tax on gains |

| Wants all three benefits | PPF + NPS + ELSS combo | Use EPF for base safety, ELSS for 80C limit, NPS for extra Rs 50K deduction, PPF for additional safe savings |

PPF — Public Provident Fund 2026

What Makes PPF Unique

PPF is the only investment in India that is EEE — Exempt at investment (80C deduction), Exempt on returns (interest not taxed), and Exempt at maturity (full withdrawal tax-free). No other mainstream investment offers this triple tax exemption.

| PPF Feature | Details 2026 |

| Current interest rate | 7.1% per annum (reviewed quarterly by government) |

| Lock-in period | 15 years — partial withdrawal allowed from year 7 |

| Annual investment limit | Minimum Rs 500, Maximum Rs 1,50,000 per year |

| Tax on investment | Deductible under Section 80C up to Rs 1.5 lakh |

| Tax on interest | Completely tax-free — no TDS, no declaration needed |

| Tax on maturity | Completely tax-free — full corpus withdrawn without tax |

| Risk | Zero — sovereign guarantee from Government of India |

| Loan facility | PPF loan available from year 3 to year 6 — up to 25% of balance |

| Extension after 15 years | Extendable in 5-year blocks — with or without fresh contributions |

| Where to open | Post office, SBI, HDFC Bank, ICICI Bank, most nationalized banks |

PPF Maturity Amount — Real Numbers

Rs 1.5 lakh invested every year in PPF at 7.1% interest for 15 years:

- Total invested: Rs 22,50,000

- Maturity amount: approximately Rs 40,68,000

- Tax-free gain: Rs 18,18,000

- Effective post-tax return: 7.1% (since no tax — real return equals stated return)

Compare this to a bank FD at 7% — the FD interest is taxed at your slab rate (30% for higher earners), making the effective post-tax return only 4.9%. PPF at 7.1% tax-free beats a 7% FD for anyone in the 20-30% tax slab.

| Tip: PPF deposit timing matters. Deposit before April 5th of each financial year to earn interest for the full year on that amount. Deposits after April 5th earn interest only from the following month. |

PPF Withdrawal Rules

- Full withdrawal: Only after 15-year maturity — or death of account holder

- Partial withdrawal: From year 7 onwards — up to 50% of balance at end of year 4 or year preceding withdrawal (whichever lower)

- Extension with contributions: After 15 years, extend in 5-year blocks — continue depositing, continue earning tax-free interest

- Extension without contributions: Balance continues earning 7.1% tax-free without any new deposits — good passive wealth option

NPS — National Pension System 2026

What Makes NPS Unique

NPS is India’s government-regulated pension scheme offering the highest combined tax benefit of any investment — Rs 2 lakh in deductions if you use both 80C and 80CCD(1B) together. The trade-off is mandatory annuity purchase at retirement — you cannot withdraw the entire corpus at once.

| NPS Feature | Details 2026 |

| Tax benefit on contribution | 80C: up to Rs 1.5 lakh. 80CCD(1B): additional Rs 50,000 — total Rs 2 lakh deduction possible |

| Employer contribution benefit | Up to 10% of Basic salary — deductible under 80CCD(2), available in both old and new tax regime |

| NPS Tier 1 vs Tier 2 | Tier 1: mandatory lock-in till 60, tax benefits apply. Tier 2: voluntary, no lock-in, NO tax benefits |

| NPS equity allocation | Active choice: up to 75% in equity (E), rest in corporate bonds (C) and government securities (G) |

| Expected return | 10-12% CAGR historically for aggressive (75% equity) allocation |

| Exit at age 60 | Minimum 40% must be used to buy annuity (monthly pension). Up to 60% withdrawn as lump sum — tax-free |

| NPS partial withdrawal | Allowed after 3 years of contribution for specific reasons: home, education, critical illness, disability |

| Tax on lump sum at exit | 60% lump sum withdrawal is completely tax-free. 40% annuity income taxed as per slab |

| NPS exit rules before 60 | If exit before 60: minimum 80% must go to annuity. Only 20% lump sum — not recommended |

| Minimum contribution | Rs 500 per year Tier 1 minimum to keep account active |

NPS Annuity Rules — The Most Misunderstood Part

Many people avoid NPS because of the annuity requirement. Here is the reality:

At age 60, you withdraw 60% as a tax-free lump sum and use the remaining 40% to buy an annuity from an IRDAI-registered insurance company. The annuity pays you a monthly pension for life.

Example: Rs 1 crore NPS corpus at 60. You withdraw Rs 60 lakh tax-free. Rs 40 lakh buys annuity at approximately 6-7% annuity rate = Rs 20,000 to Rs 23,000 per month for life.

The pension is taxable as income. But you also have Rs 60 lakh lump sum — which you can reinvest in Senior Citizen Savings Scheme or debt mutual funds for additional income.

| Tip: NPS is most powerful when your employer contributes to Tier 1. The employer contribution (up to 10% of Basic) is deductible under 80CCD(2) in BOTH old and new tax regimes — making it one of very few deductions that survives the new regime. |

ELSS — Equity Linked Savings Scheme 2026

What Makes ELSS Unique

ELSS is the only 80C investment with full equity exposure and the shortest lock-in period. It is not a retirement product — it is a wealth creation product that also gives 80C benefit as a bonus.

| ELSS Feature | Details 2026 |

| Lock-in period | 3 years per instalment — shortest in all 80C options |

| Expected return | 12-16% CAGR over 7-10 year horizon (market-linked, not guaranteed) |

| Tax on investment | Section 80C deduction up to Rs 1.5 lakh |

| Tax on gains | LTCG: 10% on gains above Rs 1.25 lakh per year after 3-year lock-in |

| Risk | Equity market risk — portfolio can fall 20-40% in bad years |

| Liquidity after lock-in | Full — redeem any amount anytime after each unit completes 3 years |

| Best horizon | 7 years minimum, ideally 10-15 years for best results |

| Who manages it | Professional fund manager — SEBI regulated AMC |

| SIP option | Yes — Rs 500/month minimum, each instalment has own 3-year lock-in |

| Return guarantee | No guarantee — returns depend on equity market performance |

ELSS Returns — What 15 Years Actually Looks Like

Rs 1.5 lakh invested annually in ELSS for 15 years at 13% CAGR (conservative long-term equity assumption):

- Total invested: Rs 22,50,000

- Maturity corpus: approximately Rs 67,50,000

- Gain: Rs 45,00,000

- Tax on gains: 10% LTCG on gains above Rs 1.25L per year — approximately Rs 2-4 lakh total depending on withdrawal timing

- Net corpus after tax: approximately Rs 63-65 lakh

| ELSS beats PPF by Rs 23-25 lakh over 15 years on the same Rs 1.5 lakh annual investment — but PPF gives guaranteed Rs 40 lakh while ELSS gives probabilistic Rs 63-65 lakh. The extra Rs 23 lakh comes with equity market risk. Your risk tolerance decides which is right. |

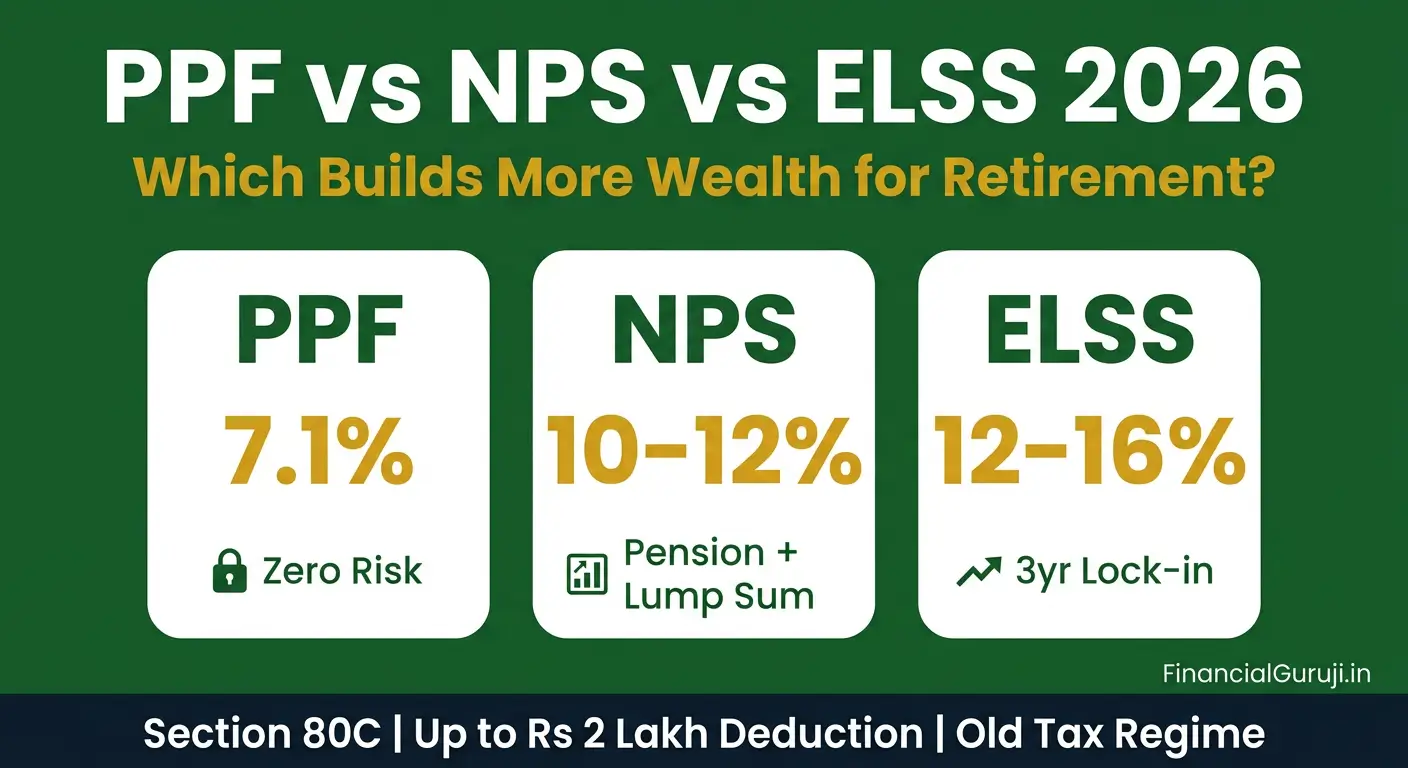

PPF vs NPS vs ELSS — The Master Comparison Table

| Factor | PPF | NPS (Tier 1) | ELSS |

| Annual 80C deduction | Up to Rs 1.5L | Up to Rs 1.5L + Rs 50K extra (80CCD1B) | Up to Rs 1.5L |

| Lock-in | 15 years | Till age 60 | 3 years per SIP |

| Expected return | 7.1% (guaranteed) | 10-12% (equity allocation) | 12-16% (equity) |

| Return guarantee | Yes — sovereign | No — market-linked | No — market-linked |

| Risk level | Zero | Low to Medium | Medium to High |

| Tax on maturity | 100% tax-free (EEE) | 60% tax-free, 40% annuity taxed | 10% LTCG above Rs 1.25L |

| Liquidity | Partial from year 7 | Partial after 3 years (limited reasons) | Full after 3 years |

| Retirement suitability | Excellent — safe corpus | Excellent — pension + lump sum | Good — wealth building |

| New regime benefit | No (80C not available) | Yes — 80CCD(2) employer contribution | No (80C not available) |

| Best age to start | Any age | 25-40 for maximum benefit | Any age with 7yr+ horizon |

Which Combination Works Best — By Investor Type

| Investor Profile | Recommended Allocation | Reasoning |

| 25-35 years, salaried, old regime, long horizon | ELSS Rs 1.5L + NPS Rs 50K extra (80CCD1B) | Maximum deduction (Rs 2L), highest growth, time to ride equity cycles |

| 35-45 years, salaried, wants balance | ELSS Rs 1L + PPF Rs 50K | Growth via ELSS, safety via PPF, fills 80C limit with diversification |

| 45-55 years, approaching retirement, risk-averse | PPF Rs 1L + NPS Rs 50K (80CCD1B) | Guaranteed returns + pension structure, reduced equity exposure |

| Any age, new tax regime | NPS via employer (80CCD2) only | Only NPS employer contribution survives new regime — rest of 80C not available |

| Self-employed, old regime | ELSS Rs 1.5L + NPS Rs 50K (80CCD1B) | Same maximum deduction benefit as salaried — NPS open to self-employed too |

PPF Extension After 15 Years — The Hidden Strategy

Most people withdraw PPF at 15 years. The smarter move: extend without contributions.

After 15 years, you can extend your PPF account in 5-year blocks without making any new deposits. Your existing balance continues earning 7.1% tax-free interest. You can withdraw any amount once per year during the extension period.

This turns PPF into a tax-free emergency fund and retirement income source simultaneously — no other instrument offers this combination of liquidity, safety, and tax-free returns.

Use our PPF Calculator, NPS Calculator, and SIP Calculator to compare your exact corpus across all three options

Frequently Asked Questions

Can I invest in all three — PPF, NPS, and ELSS — at the same time?

Yes, absolutely. PPF and ELSS both fall under the Rs 1.5 lakh Section 80C limit — so the combined investment in both cannot exceed Rs 1.5 lakh for 80C benefit. NPS Tier 1 under 80CCD(1B) gives an additional Rs 50,000 deduction completely separately. So the maximum combined deduction is Rs 2 lakh (Rs 1.5L under 80C + Rs 50K under 80CCD1B).

PPF vs NPS — which gives more money at retirement?

NPS with 75% equity allocation historically gives higher corpus than PPF over a 20-30 year period due to higher expected returns (10-12% vs 7.1%). However, NPS requires 40% annuity purchase. If you compare net withdrawable lump sums: NPS 60% lump sum vs PPF 100% lump sum — PPF may actually give more accessible money, especially if NPS corpus is large.

What is NPS Tier 2 and is it worth investing?

NPS Tier 1 vs Tier 2: Tier 2 is a voluntary savings account linked to NPS with no lock-in and no tax benefits (except for central government employees). Since Tier 2 has no tax advantage and no lock-in, it offers no benefit over a regular mutual fund. For most investors, Tier 2 is not worth using — invest in direct mutual funds instead.

Can I withdraw PPF before 15 years for emergency?

Full withdrawal before 15 years is not allowed except on death of account holder. However, PPF loan is available from year 3 to year 6 (up to 25% of balance). Partial withdrawal is allowed from year 7 onwards (up to 50% of balance). For genuine emergencies, the year 7 partial withdrawal option is useful.

Is ELSS better than PPF for someone aged 40?

At age 40 with a 20-year retirement horizon, ELSS still has strong potential to outperform PPF. The key question is risk tolerance. If you can stay invested through market corrections without panic-selling, ELSS historically delivers meaningfully higher corpus. If market volatility causes you stress or you might withdraw early, PPF’s guaranteed 7.1% tax-free is the better choice.

What happens to NPS if I die before age 60?

In case of death of the NPS subscriber before age 60, the entire accumulated corpus is paid to the nominee as a lump sum — no annuity purchase required. The nominee can withdraw 100% tax-free. This makes NPS less risky from a death-before-retirement perspective than most people assume.